| home |

Finance and Statistics - Kovalev AM

12.3 SECURITIES JOINT STOCK COMPANY

Action - type of security, output AO. She suggests making certain funds in property and stock ownership certifies its holder to a share in the authorized capital. The action gives its owner the right to receive part of the profit (dividend) from JSC activity and, as a rule, to participate in its management.

The shares do not have a certain period of treatment, ie They are perpetual. The share is indivisible, but may belong to more than one person on the common ownership.

All information issued shares are included in the prospectus, which is detected by the relevant government authorities, as provided for by the legislation of the Russian Federation on securities. Shares that are not registered in the prescribed manner, shall be deemed invalid.

The shares acquired by the shareholders, are placed. Shares issued in addition, called the announcement. Number and par value of both, as well as the procedures and conditions of their placement are determined by the company charter.

Types of shares. The shares issued by the company are classified primarily in common and preferred.

Ordinary shares are entitled to vote at the general meeting of shareholders (one share - one vote). The holders of ordinary shares participate in the profits of joint-stock company only after the replenishment of reserves and payment of dividends on preferred shares. Therefore, the payment of dividends on ordinary shares is not guaranteed as it depends on the outcome of commercial activity and the amount of profits.

Upon liquidation of the Company's ordinary share gives the shareholder the right to part of the property stock after settlements with creditors and the holders of preferred shares.

Preferred shares are of several types. In accordance with the Regulations on the commercialization of state-owned enterprises with a simultaneous conversion into open joint stock companies, approved by Presidential Decree July 1, 1992, issue preference shares of two types - A and B.

There cumulative preference shares, convertible into common or preferred other types of redeemable (callable), preferred stock sinking fund, voting and non-voting preference shares, and other. The number and nominal value of issued shares of each of these types is placed so and declared, determined by the charter of the joint-stock company.

Preferred shares have no voting rights at the General Meeting of Shareholders (unless otherwise stipulated by the law on joint-stock company or the company's charter for a particular type of preferred shares). Nevertheless, holders of preferred shares have the advantage over the holders of common shares in the distribution of income and property in the event of liquidation of the company.

Cumulative preference shares - these shares on which any unpaid or partially paid dividend provided for in the statute, accumulated and paid subsequently.

Preferred shares have a fixed dividend, the amount of which is determined by their release. Payments to holders of preferred shares are made primarily to the payments to the holders of ordinary shares. Characteristically, according to the law on joint stock companies the founders of society can expand the rights of shareholders - holders of preferred shares, as for any type of preference shares shall be established by a different scope of rights, a different order of priority of payment of dividends and liquidation value.

Owners of some types of preference shares (ie, cumulative) got the right to participate in general meetings of shareholders with voting rights. However, this right is temporary in nature, ie, terminated upon fulfillment of their public commitments to the payment of dividends. In addition, owners of certain types of preferred shares have a permanent right to vote in the discussion of the general meeting of shareholders of certain legal issues AB. In addressing issues of reorganization and liquidation of the Company at general meetings of the shareholders participating in the voting power all holders of preferred shares. Preferred shares are usually issued with a small nominal value to attract small investors, so in dealing with the important issues of the JSC and the management of its assets remains a priority for large investors who hold large blocks of common stock.

Registered shares and bearer shares. In accordance with the Russian joint-stock companies current legislation have the right to issue only registered shares. The holders of such shares are registered in a special register.

Action bearer means the free sale and purchase of it by mutual agreement of the parties, without any registration, despite the simple process of handling such shares, they are not widely used in the world, including in Russia, due to significant difficulties in the management of the property stock when using them. The presence of uncontrolled movements of the share capital of the process extremely negative consequences may result in the absence of mandatory registration of transactions sale and purchase of bearer shares.

The value of shares. There are several types of value of shares: nominal, and the emission market.

The nominal value of the shares indicated on the form of shares is determined by dividing the amount of the authorized capital stock in the amount

honors issued shares. For example, if the authorized capital stock of 600 thousand. Rub. and issued 300 thous. ordinary shares, the nominal value of one share is 2 rubles. (600,000: 300,000).

According to the founders of the nominal value of paid shares of the Company at its establishment. The nominal value of a share is the basis for the determination of emission and the market value, as well as calculating the dividend. At the par value of the shares is determined by the proportion of shareholders in the payment of his assets in case of liquidation of the JSC.

The price at which the issuer sells a share investor defines its issue price. This cost may or may deviate from the nominal value in either direction. Thus, the State Privatization Program for 1992 included the first and second embodiments of benefits for members of the workforce. Those of them who have chosen the first option, up to 10% of the shares were sold at a discount of 30% of par value. Consequently, emission was below the nominal value in this case.

Officials of the administration of JSC was granted the right to acquire a 5% stake at nominal value. In this case, the emission and the nominal price match,

When selecting the members of the staff of the second variant of the benefits 51% of the shares purchased by them was estimated at nominal value, increased by 1.7 times. In this case, the emission value exceeds the nominal.

The price at which the action is implemented on the stock exchange and in the OTC market, determine its market value.

The market value depends on the ratio of supply and demand, which in turn is determined by many factors: the influence of advertising, stock market conditions, and especially the size of the dividend on shares and. the level of bank interest. The higher dividend rate, the greater the market value of the shares, and vice versa. The higher the level of bank interest, the lower the market value of the shares.

In accordance with the JSC Law Society has the right to place an additional issue of ordinary shares at a price below their market value by 10% of the company's shareholders pre-emptive right to acquire such shares. In addition, below the market value of the additional shares with the participation of the intermediary can be accommodated. In this case, the market value decreases by more than the value of remuneration mediator.

In order to determine the course of action, should be the market value of the stock divided by the par value and multiply by 100. For example, the share of a nominal value of 5 rubles. sells for

Bridges in this case is greater than the nominal 1.5 times.

Bridges in this case is greater than the nominal 1.5 times.

The relative height of the course can be judged against the market price of the shares to the amount of profit per share. This value is called coefficient of "course / income". Growth or fall of this factor in the stock market indicates a rise in price or falling share price as a result of changes in the economy, stock market activity, the Bank's accounting rate and many other factors.

Share certificate - is a security evidencing the ownership of the said person a certain number of shares. Shares are generally not stored in the hands of shareholders. Instead, the owners receive shares of one or more share certificates - documents proving their ownership. One sergifikat issued free of charge on fully paid shares held by the shareholder at the time of the creation of joint-stock company. The rest of the certificates can be issued to the shareholder at his request, for a fee determined by the Board of Directors.

The transfer of ownership of Shares in the transfer certificate is considered valid if performed registration in the prescribed manner. Share certificate has the following details:

- Title of the document;

- the name and location of the company;

- category (a series of) shares, ownership of which is certified by the certificate and the associated rights and restrictions;

- a nominal value of one share of this category;

- the amount and number of shares, ownership of which is certified by the certificate, and their total nominal value;

- name (name) and location (residence) of the shareholder;

- dividend rate (for a fixed dividend);

- signatures of two responsible persons of the company;

- Society seal.

In the absence of one of these requisites share certificates are invalid.

Dividend - income from shares, paid by a portion of net profits to be distributed among its shareholders, per share, the dividend can be expressed as an absolute amount and as a factor. Factor, or the percentage of the dividend rate, defined as the ratio of dividend income in monetary terms to the nominal value of the shares. The interest rate determines the dividend yield of the stock.

Dividends can be paid not only in money, but also paid for other commodity-material assets in cases stipulated by the company charter.

on outstanding shares Dividends may be paid in accordance with the decision of the shareholders and the Charter of JSC quarterly, semiannually or annually. Dividends are paid from the net profit for the current year. Interim dividends paid by the decision of the Board of Directors, and the size and form of payment of dividends are determined by resolution of the general meeting of shareholders. The volume of annual dividends may not be less than the amount paid interim dividends and greater than the sum of dividend recommended by the Board of Directors.

Procedure for payment of the dividend depends on the type of shares. First of all dividends paid on preferred shares. According to preferred shares of certain types of dividends may be paid by a specially created from the net profit funds.

Characteristically, the JSC Law provides for the right of the general meeting of shareholders' to decide to pay dividends on certain categories of shares, moreover, on partial payment of dividends on preferred shares, even if the available balance of net profit. Such a decision may be quite legitimate in connection with the direction of funds for investment and other purposes related to the development predprinimatblskoy of society.

Dividends on types of shares is made in the established order. The first dividend is paid on preference shares with preferential dividend type size fixed in the statutes. For example, the Regulation on the commercialization of public enterprises with a simultaneous conversion into open joint stock company stipulated that on preferred shares of type A and B dividends are calculated as follows. For each type A share dividend is calculated at a rate of 10% of net profit of JSC on the results of the last fiscal year, divided by the number of shares constituting 25% of the share capital of the company.

For each share of type B the dividend is determined in the amount of 5% of net profit of JSC on the results of the last fiscal year, divided by the number of shares constituting 25% of the share capital of the company. If a dividend on each preferred share of type A and B is lower than the dividend for each ordinary share, the dividend on the preference shares is filled to the size of the dividend on ordinary shares.

Next, the dividends paid on the types of preferred shares in the order of preferential rights to these shares. Finally, the dividends paid on preference shares without fixed dividend in the amount of the charter.

After full payment of dividends provided for society for all types of preferred stock dividends are paid on common shares. Dividends on ordinary shares can not be paid in the event of financial difficulties in obtaining insufficient amount of profit, and, as noted above, in connection with the direction of funds for the development of economic activity.

The actual amount of dividends declared for the year by the General Meeting of Shareholders on the proposal of the Board of Directors. According to shares issued into circulation or on the balance of stock, dividends are not paid. Dividends will not be paid also to the full implementation of the company conditions of compulsory redemption of shares from its shareholders.

The Company Law, in accordance with the Civil Code provides that the payment of dividends can be carried out after full payment of the authorized capital of the company and provided that the net asset value after the stock dividend payment must be greater than the size of the authorized capital and reserve fund.

Dividends will not be paid if the identified signs of insolvency (bankruptcy) of the company or such signs appear as a result of the dividend payment.

Examples of determining the dividend.

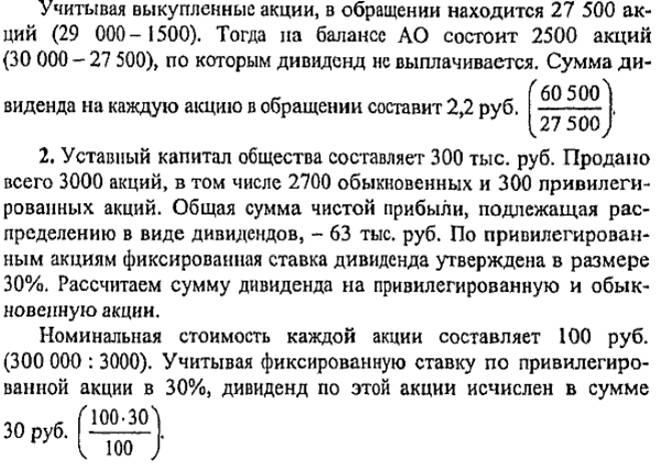

1. From the registered joint-stock company 30 thousand. 29 thousand ordinary shares. Selling Shareholder. Subsequently, the company has repurchased 1,500 shares from the owners. As a result, the shareholders' meeting decided to distribute 60.5 thousand. Rubles, net profit as dividends.

Consequently, the dividend will be paid to all preferred shares in the amount of 9,000 rubles. (30 • 300). The remaining profit for payment of dividends on ordinary shares 54 000 rubles. (63 000 - 9000). Consequently, for each common share dividend of 20 rubles. (54000: 2700).

Benefits of the sale of shares in the process of corporatization. In accordance with the Presidential Decree "On the main provisions of the State program of privatization of state and municipal enterprises in the Russian Federation after July 1, 1994" dated July 22, 1994, №1535 company in the process of incorporation at the general meeting of the staff take a decision (at least 2 / 3 votes) of the benefits you select. There are three options.

• According to the first embodiment of the persons entitled to benefits receive free registered preferred shares, amounting to 25% of the share capital, but not more than 20 times the minimum wage established by law per employee. In addition, by closed subscription sold ordinary shares (with voting rights), constituting up to 10% of the share capital, but in an amount not more than b times the minimum wage per employee.

These shares are sold at a discount of 30% of par value, with the installment of up to three months, but the amount of down payment shall not be less than 50% of the shares.

Administration of privatized enterprises have the right to acquire ordinary shares in the amount of up to 5% of the share capital, but not more than 200 times the minimum wage per person.

- In a second embodiment of all of the staff members have the right to acquire ordinary (voting) shares, which share in the authorized capital of up to 51%. The sale of shares on preferential terms, and their gratuitous transfer is not carried out.

- In a third embodiment of a group of founders of the company, taking over with the consent of the general meeting of the collective responsibility for the implementation of the privatization plan and the avoidance of bankruptcy for a period not exceeding one year, entitled after a specified period and under specified conditions to acquire ordinary (voting) shares, constituting 30% of share capital. During the year, these persons have the right to vote the ordinary shares held by the Fund property. However, they are responsible for the commitments with their personal assets and guarantee insertion of at least 200 times the minimum monthly wage per each member of the group.

Всем работникам предприятия с учетом членов указанной группы продаются обыкновенные (с правом голоса) акции, доля которых в уставном капитале составляет 20%, но не более 20-кратного размера минимальной месячной оплаты труда в расчете на одного работника. Данные акции продаются со скидкой 30% их номинала с предоставлением рассрочки на три месяца. Первоначальный взнос не может быть меньше 25% стоимости акций.

Если группа учредителей, взявших на себя обязательства по осуществлению плана приватизации, не выполнит обязательств, акции, которые предназначались к продаже им, подлежат реализации населению на аукционах.

Облигации и проценты по ним. Иные ценные бумаги. Облигационный заем - это форма выпуска облигаций акционерным обществом на определенных, заранее оговоренных правовых условиях.

Путем выпуска облигационных займов АО привлекает в оборот заемный капитал. Порядок и условия выпуска облигационных займов определяются общим собранием акционеров. Выпуск облигационного займа производится по решению совета директоров, если иное не предусмотрено уставом АО.

Общество вправе выпускать облигационные займы без поручительства и с поручительством. В последнем случае оговаривается размер имущества, на которое владельцы облигаций имеют права залогодержателя или обязательства поручителя (гаранта) данного облигационного займа.

Облигационные займы без поручительства или гарантии третьих лиц могут быть выпущены не ранее чем через два года после успешной деятельности АО. Общая сумма облигационного займа не должна превышать величину уставного капитала АО или сумму обеспечения, предоставленного обществу третьими лицами.

Облигация - это ценная бумага, представляющая собой долговое обязательство акционерного общества уплатить владельцу облигации в установленный срок номинальную стоимость или номинальную стоимость с процентами. Облигации выпускаются после полной оплаты уставного капитала. Держатели облигаций в отличие от владельцев акций не являются собственниками акционерного общества, а становятся его кредиторами.

Тем не менее держатели облигаций имеют определенные преимущества перед акционерами. Выплата процентов по облигациям производится не реже одного раза в год независимо от величины прибыли и финансового состояния общества, т.е. до начисления и выплаты дивидендов по акциям. При ликвидации АО держатели облигаций имеют преимущественное право по сравнению с акционерами на активы общества.

Общество имеет право выпускать облигации трех типов: обеспеченные залогом имущества, под обеспечение, предоставленное третьими лицами, и без обеспечения.

Законом об АО и в соответствии с Гражданским кодексом РФ возможность выпуска облигаций при отсутствии обеспечения предусмотрена не ранее третьего года существования АО и при условии утверждения к моменту выпуска облигаций двух годовых балансов АО.

Облигации по желанию владельцев могут 'быть погашены досрочно, но не ранее срока досрочного погашения, обусловленного в решении о выпуске облигаций.

Учитывая, что акции и облигации являются ценными бумагами АО, предусмотрена возможность выпуска конвертируемых облигаций, которые по решению общего собрания при определенных условиях могут обмениваться на акции. Однако облигации, конвертируемые в акции, не могут быть размещены обществом, если количе-

ство объявленных акций меньше количества акций этих типов, право на приобретение которых имеют данные облигации.

При всей важной роли облигаций как дополнительной возможности привлечения денежных средств для расширения акционерной деятельности обращение облигаций на российском рынке ценных бумаг до настоящего времени не получило должного развития.

Облигации могут быть именными и на предъявителя. Владельцы именных облигаций регистрируются обществом в специальном реестре. В связи с этим обладатель именной облигации обязан своевременно извещать общество об изменении сведений, включенных в реестр. Реквизитами именной облигации являются:

в номер облигации;

в номинальная стоимость;

» размер процентной ставки;

» имя держателя.

При потере именной облигации права владельца возобновляются за определенную плату.

Облигации на предъявителя называют купонными, так как обладатель такой облигации может получить проценты по предъявлении купонного листа, прилагаемого к облигации. АО, эмитирующее облигации на предъявителя, не ведет учет их владельцев. Облигации на предъявителя имеют следующие реквизиты:

в название общества эмитента;

» общую сумму займа;

» условия и порядок выплаты процентов.

При утере облигации на предъявителя права владельца восстанавливаются в судебном порядке.

Сертификат облигаций - это ценная бумага, удостоверяющая количество и вид принадлежащих обладателю именных облигаций. Если сертификат свидетельствует о праве обладания одной облигацией, он может именоваться облигацией. В случае продажи зарегистрированных облигаций новому владельцу выдается новый сертификат с погашением ранее выданного сертификата. Сертификат облигаций имеет следующие реквизиты:

в наименование ценной бумаги;

в наименование и местонахождение АО;

® дату выпуска и общую сумму облигационного займа, серии облигаций и связанные с этим права;

в срок погашения облигационного займа;

в номинал одной облигации;

в количество и номера облигаций, владение которыми удостоверяет сертификат, и их общую номинальную стоимость;

- наименование и реквизиты лиц, предоставляющих обеспечение займа - при выпуске займа под обеспечение третьих лиц;

- размер и порядок исчисления процентов по облигациям и порядок их выплаты;

- подписи двух ответственных лиц общества; ® печать общества.

Проценты по облигациям выплачиваются в преимущественном порядке по сравнению с дивидендами по акциям. Проценты рассчитываются по отношению к номинальной стоимости облигаций независимо от их, курсовой стоимости. При первичном размещении облигаций в первый год функционирования АО проценты выплачиваются пропорционально времени фактического обращения облигации (если иное не предусмотрено условиями выпуска).

Проценты по облигациям являются фиксированными либо незначительно изменяются в зависимости от срока их обращения и погашения займа. Выплачиваются проценты за счет чистой прибыли АО (до выплаты дивидендов по акциям), а при ее недостатке - из резервного фонда.

Выплата процентов производится непосредственно АО, выпустившим заем, либо банком-агентом, либо финансовым посредником за вычетом соответствующих налогов. Выплата процентов по облигациям производится, как правило, безналичным путем: с помощью чеков, платежных поручений, почтовых или телеграфных переводов.

Условиями выпуска займа выплата процентов может быть предусмотрена в виде денег, ценных бумаг, товаров и имущественных или иных прав, имеющих денежную оценку. При выплате дохода на облигации делается отметка о выплате процентов путем погашения или отрезания купона (на облигациях на предъявителя). Выплата процентов не производится, если это указано в облигации и стоимость эмиссии ее меньше номинальной стоимости.

Проценты по облигациям могут выплачиваться один раз в квартал, полугодие или год. Если АО отказывается выплатить проценты в установленный срок, оно может быть признано несостоятельным и ликвидировано. Имущество неплатежеспособного эмитента может быть использовано для выплаты процентов по облигациям.

Пример определения годового дохода по облигации.

Именная облигация имеет номинальную стоимость 100 руб. Процентная ставка по облигациям установлена в размере 50% годовых. Текущий годовой доход по облигации составит 50 руб. (100-5)/100

Иные ценные бумаги. Акционерное общество вправе размещать не только акции и облигации, но и другие виды ценных бумаг. Гражданским кодексом РФ, Федеральным законом об АО и другими нормативными правовыми актами регулируются общие правила выпуска, размещения и обращения ценных бумаг,

К долговым ценным бумагам, кроме облигаций, относятся векселя, депозитные и сберегательные сертификаты банков. Вексель удостоверяет безусловное денежное обязательство векселедателя уплатить векселедержателю определенную сумму денег в установленный срок. Сберегательный сертификат - это письменное свидетельство кредитного учреждения о депонировании на определенный срок денежных средств вкладчика, а именно физического лица, с безусловным обязательством возврата вклада с установленным процентом. Депозитный сертификат также удостоверяет аналогичное право вкладчика, в роли которого выступает юридическая организация.

Ценной бумагой является чек, используемый как платежное средство. Чек - это письменное распоряжение чекодателя организации-плательщику -выплатить чекодержателю указанную сумму денег.

К ценным бумагам относится коносамент, выражающий право собственности на конкретный товар в процессе морской перевозки. Коносамент выдается после получения товара перевозчиком груза отправителю с указанием грузополучателя.

К производным ценным бумагам относятся опционы, фьючерсы и другие, обращение которых с развитием финансового рынка в России получает все большее распространение, так как способствует вовлечению в финансовый оборот дополнительных капиталов.

Comments

Commenting, keep in mind that the content and the tone of your messages can hurt the feelings of real people, show respect and tolerance to his interlocutors, even if you do not share their opinion, your behavior in terms of freedom of speech and anonymity offered by the Internet, is changing not only virtual, but real world. All comments are hidden from the index, spam control.