| home

|

Encyclopedia of Accounting - Gracheva R.E. Section II P.1

Disposal of fixed assets

The tax aspect . When accounting for the sale of fixed assets in accounting, all tax consequences arising from such transactions should be taken into account. To a large extent, this concerns the formation of gross revenues and gross expenses in order to determine the tax base for calculating the profit tax.

First of all, we determine to which group of fixed assets are the objects to be sold. In particular, if such objects belong to Group I, then gross proceeds include the amount of excess of proceeds from the sale of the object over its book value (residual) value (It is worth recalling that the term "book value" in its tax sense is very different from the similar term applied In any case, if we are talking about tax accounting, remember that the balance here is useless.)

At sale of the objects concerning II, III or VI group, - for the sum of sale cost of these objects the book value of the corresponding group decreases. This is the case when the balance of book value is possible, beyond which there is no physical unit; In this case in the next quarter this "non-embodied" balance is attributed to gross expenses (see subparagraph 8.4.7 of the Law). Just as it is entirely possible that physical units have remained, and the cost has been exhausted. Consequently, in cases when the next sale is that there is nothing to reduce (that is, when the sales value exceeds the balance of the book value while the physical units are available), the book value of the remaining objects is equated to zero, and the excess amount is included in Gross income (see subparagraph 8.4.4 of the Law). The same should be done when determining the book value of groups in the case of the imposition of fixed assets in the authorized capital of other enterprises (paragraphs 8.4.1).

Thus, the difference between the reflection of the sale of fixed assets of group I from the sale of fixed assets of other groups in tax accounting is that gross income as a result of such operations with objects of group I is recognized at the time of sale of each object. And when selling objects belonging to other groups, the gross income for each sale case can not be determined (tax accounting for these groups is not conducted on-object basis). Consequently, he is recognized in the whole group, when the time comes. This time can wait for years. And this is not bad from the point of view of minimizing the tax base.

As for the value-added tax, we recall that, according to subpar. 3.1.1 Art. 3 of the Law on Value Added Tax, sales of fixed assets are subject to VAT. At the same time, the tax base is determined on the basis of contractual (contract) value, determined at free or regulated prices.

Accounting aspect . Sale of fixed assets is reflected in the accounting according to the following algorithm: see Chart 2.1.

Scheme 2.1

ACCOUNTS AND EVENTS

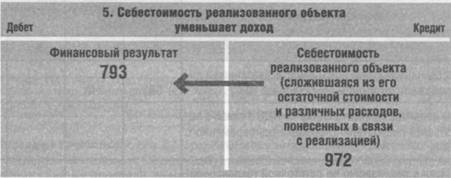

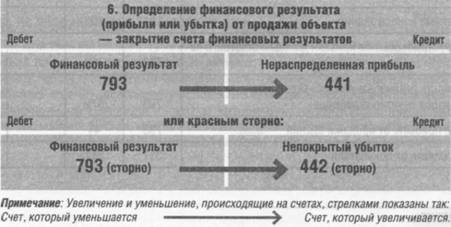

Scheme 2.1 (however, like all the others shown in the tables below) can be described in a few words: an object is transferred - its value is written off from the balance, this cost - together with the costs incurred by the enterprise in connection with such a sale - reduces the revenues received From the buyer (or accrued to receive), the remaining income - profit (or loss, if the expenses exceeded revenues). Everything else that can happen during such operations is also reflected only "what I see is what I write". Nothing that does not really happen in the accounting entries should not be. This also applies to the charging of various kinds of taxes and fees that result from certain operations. After all, in order to pay the tax, you should accrue such obligations to the budget.

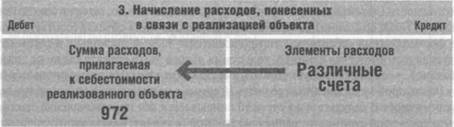

All the following schemes are similar to each other and at the same time different. They are similar in that they all reflect one thing - the sale of fixed assets. And different because these objects belong to different groups, and therefore, are accounted for in different sub-accounts. And they differ in the sequence of operations (prepayment and further accompanied by various operations for the calculation of VAT) and the composition of costs, of which the cost of the realized object was formed. In some cases, this cost consists of a single element - the residual (balance) value of the sold object, in others - other than this cost, the implementation cost includes other expenses incurred in connection with the disposal of the object.

To correctly reflect the operations that occur with fixed assets, we should not forget that the economic operation is primarily an event. Therefore, the accounting entries should reflect the event. Take for example some of the events shown in Scheme 2.1.

Account 361 is the buyer's account.

Account 742 is the seller's revenue account, that is, the means that the seller expects to receive from the buyer in exchange for the assets transferred to him. This posting (Д-т 361 К-т 742) shows the exchange, to be exact, its beginning (if payment has not yet arrived) or completion (if the buyer has paid before). This is an exchange between the buyer and the seller.

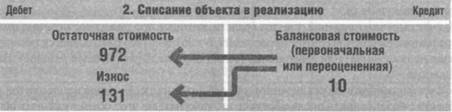

Account 972 is the account for the formation of the selling price. And one of the elements of this cost price when the object is written off the balance sheet (after all, after transferring it to the buyer, this object no longer meets the criterion for recognizing the asset), its book value must necessarily become its value. On the balance sheet, fixed assets are shown at a residual value (original (it is also overvalued) minus depreciation). Therefore, at the residual value, this object must be written off. Such write-off is carried out from the credit of the account of the object (corresponding subaccount of account 10) to the debit of the cost of sales account (account 972). And since in this case the object disappears as a physical and a value unit, then the amount of depreciation of this object also should not be taken into account on the balance sheet from now on - it should also be written off together with the object. On this basis, and conducts the commissioning of the 131-K-t engine 10, to which the undersigned from the account 10 is ultimately written off for a decrease in such a contract as "wear." As a result, the entire initial cost of the retiring object is written off from account 10, because part This value, equal to the residual (and, therefore, balance sheet), became the basis for the formation of its realizable cost, and the rest, equal to the amount of depreciation, reduced this contract on the balance sheet by exactly the amount that was left with the object.

Comments

When commenting on, remember that the content and tone of your message can hurt the feelings of real people, show respect and tolerance to your interlocutors even if you do not share their opinion, your behavior in the conditions of freedom of expression and anonymity provided by the Internet, changes Not only virtual, but also the real world. All comments are hidden from the index, spam is controlled.