| home

|

Theory of the accounting region - Vasyuta-Berkut O.I.

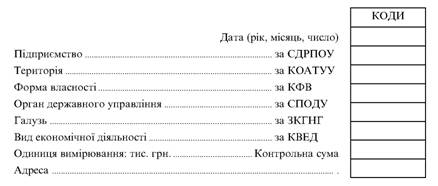

Додаток 2 Положиня (стандарт) бухгалтерського обліку Balance sheet

ЗАТВЕРДЖЕНО Міністерством фінансів України order for 31 berezney 1999 rub. No. 87

REGISTERED

In the Ministry of Justice of Ukraine

21 червня 1999 р. For No. 396/3689

Poslozhnya (standard) of the accounting region 2 "Balance"

Загальні положення

1. Tsim Poslozhnyam (standard) viznachayutsya zmist і form of balance that zagalnyi vimogi before yokogo yogo articles.

2. Normative Standard (standard) zastosovuytsya to the balance of payments, organisatsiyi and іnshih juridicheskih osib (dalі - pіdpriєmstva) usіh forms of power (krім bankів і budgetary installations).

3. Specificity of the warehouse consol idovanogo balance viznachayutsya okremim posozhnyam (standard).

4. Termini, scho vikoristovuyatsya in ts'omu Poslovennі (standardі), мають таке значення:

Activi - resource, control over the performance of the results of past podi, vikoristannya yakih, yak ochikuyutsya, bring to nadohodzhennya ekonomichnyh vigod u Maybutnomu.

Vlasny kapital - part of the assets of consumption, sho zalishaetsya pislja virahuvannya yogi zobov'azan.

Dovgostrokov zobov'yazan'ya - vsya zobov'yanya, yakі not ¬ by streaming zobov'yazni.

Пов'язані Parties - підприємства, стосунки між якими обумовлюють одливістьї інії іннянівівівівівів іншу піді здійснювати сутєвий впвів прийняття фінансових і оперативних рішень іншою стороныною.

Zobov'yannya - zaborgovinist pidpriemstva, yak vikikla vnasledok short minks and redemption anchovy, yak ochikuyutsya, prizvede to zmenshennya resursiv pidpriemstva, scho vtilyuyut v sobi ekonomichnyi vigody.

Еквіваленти грошових коштів - короткострокові високоліквідні фінансові інвестиції, які вільно перетоться у певні sumi грошових коштів і які characterized by an unimportant risky зміни вартості.

Фінансові інвестиції - activists, які утримуються підприємством з метю збільшення прибутку (відсотків, дивідендів тощо) та вартості капіталу або інших вигод для Інвестора.

Potoknі zobov'yаnya - zobov'yаnnya, yakі budut repaid by the extension of the operational cycle of payment of povodnіmі пінніі бути repaid in the course of two months after the beginning of the date of the balance.

Non-active activists are all activists, but not werewolves.

Turnaround activites - groshni koshti ta ek evіvalіnti, but not in vіcoristannі, and takozh іnshі activі, are recognized for realizіya chi spizhivannya in the course of the operational cycle of chi in the course of two-tenths of the months to the balance sheet.

Operatіyny cycle - promіzhok chas mіzh pridbannyam sistіv dlya zdіysnennya dіyalnі ta otrymannyam koshtіv vіd realizatsії vyroblії pro sisteії nach goodsі і послуг.

5. The method of storing the balance sheet œ nadannya koristustacham posvyїї, pravdivoї ta neperedzhennosti іnformatsії pro fіnnansovyi stn pіdpriєmstva na zvіtnu date.

6. Have a balance vіdobrazhayutsya activist, zobov'yanya that vlasniy kapital pidpriєmstva.

7. Zgortannya articles active in zobov'yazan є unacceptable, krim vypadkiv, peredbachenih vidpovidnimi positions (standards).

8. Pіsumok proizvodіv balance is guilty дорівнювати сумі зобов'язань та власного капіталу.

9. The form of the balance sheet is an addendum to that of the Posology (standard). For mali pidpriemstvom mozhe perebachatisya skorenchen form balance.

Voznachennya balance sheet items

10. The asset is reflected in the balance sheet for the name, but the yogo yogo mozhe budi dostovirno viznachena і ochikuyutsya otrimannya v majbutnomu ekonomichnyh vigod, povyazyanykh y yogo vikoristannyam.

11. Vitraty on pribbannya that securitization of the asset, as long as it does not exceed the 10th paragraph of the Provision (standard), you can not enter into the balance sheet, you can turn on the warehouse for the cost of a fixed period in the name of the financial result.

12. Zobov'yannya vіdobrazhaєtsya u balancea, yakschoo yogo otsіka mozhe budi dostovіrno viznachena ta існує дімірність зменшення економічних вигод у майбутньому внаслідок його погашення.

13. Власний капітал відображається in balance and one-time in accordance with the active principles of zobov'azan, yakі prizvodit to yogo zmіni.

Zmist articles balance sheet

14. In statti "Nematerialny activi" vіdobryazhyayut vartіst об'єктів, які віднесені to the warehouse of non-material activities in accordance with the guidelines (standards). In tsi statti, it is imposed in the first place, that is, the volatility of non-material activities, and is also accrued in the established order of sums of money. Залишкова вартість визначається як різниця між первісною вартістю і сумою зносу.

15. In stati "Unfinished budivntsvto" show vartit uncompleted budivnitsvva (vklyuchayuchi ustatkuvannya for installation), sho zdіysnyuyutsya for vlasnih needpodpriyatstva, and takozh advance payments for the financing of such budivnitsvva.

16. In statti "The basic zasobi" is imposed vartnist vlasnih and otrimanyh on the instincts of the financial leasing ob'ektiv i orendovanikh tsilinnyh mayovikh complexes, yakі vidnedeni to the warehouse of the main zgіdno zііpіdі zііpovіdnym pozhenіni (standards). At tsіt statti takozh vartity інших неиротротних матеріальних активів.

At tsі statti be imposed okremo pervisna (rezycinena) vartit, suma znosu prisposobnykh zadobiv ta ikh zalishkova vartist. Prior to the balance sheet, include Zalishkov vartit, yaka viznachaetsya yak rіznitsya між первісною (переціненою) vartіstyu zaponіv i sumoyu їh znosu na date balansu.

17. In statti "Dovgostrokov fіnansovі іnvestitsії" vіdobrazhayutsya fіnansovі іnvestitsії on perіоd more than one fate, and takozh іsі іnvestitsії, yakі not mozhut бути вільно Realize at any time. In the course of the year, visibility is determined by the method of participation in the capital, in accordance with the requirements (standards).

18. At statti "Dovgostrokova debitsorska zaborgovanist" show zaborgovannost fizichnih ta juridicheskih osib, yaka not vinikay in the course of the normal operational cycle that will be repaid in the form of two months after the date of the balance.

19. In statti "Vidstrocheni podatkovi activa" vіdobražaєtsya suma podatku na pributok, scho pідлягає відшкодуванню in the offensive perіоды унаслідок тимчасової різниці між обліковою та податковою databases оцінки.

20. The stati "Non-revolutary activists" should be given sums of non-negotiable activities, which can not be included in the wisest of articles, including "Non-negotiable activists".

21. At statti "Virbnichi zapasi" it is shown that the stock of syrovini, the basic and supplementary materials, the fowl, the purchase of spare parts, the spare parts, the tariffs, the everyday materials of the current material, the recognition for working in the normal operating cycle.

22. In statti "Tvarini viroschuvanni ta vіdgodіvli" vіdobryazhyayut vartіst dorislikh tvarin na vіdgіvіlі i v nagulі, birdsі, звірів, rabbitіv, dorislikh tvarin, vibekuvanih з basic flocks for realіzії, thіr young plants.

23. In statti "Unfinished virbitnitsu" show vitrati on the unfinished vibrobitniyu and unfinished robot (s).

24. In the statti "Ready products", show off the stock of vibrocks in the warehouse, the box of which has been closed, the yaki have passed through the viprobuvannya, priymannya, manned by the laws of the agreement with deputies, and to meet technical standards and standards. Produktsiya, yaka not vedpіdіdі nаvіnim vimogam (krіm marriage), thаt roboty, yakі not prіnjatі zamovnikom, pokazuyutsya beskladіs nezavershenogo vibrobitvtva.

25. Statti "Tovari" shows the product quality of goods, yakі pridbani pіdpriimstvami for the offensive sale.

26. In the case of "Vekselі oderzhdeni", the collection of purchases, pledges of the debitors for the products (com), vikonanot roboti nadanni sgigi, yaka is secured with bills.

27. At statti "Debtorska zaborgovannost for a friend, roboty, ambassadors" vіdobrazhaєtsya zaborgovannіst zakupitsіv abo zamovnikіv nadanі їm produktsiyu, com, roboti abo oblegi (krim zaborgovanosti, yaka pawned by a bill). At pidsumok balance is included net realizatsyna vartizhest, yaka viznachaetsya shayam virahuvannya z debіtorskoi zaborgovanostyu sumnіvnih borgiv.

28. At statti "Debtorska zaborgovannost for rozraunkami with the budget"

Show the debutor's fencing of financial and taxation bodies, and such an overpayment for handouts, gambling and other payments to the budget.

29. At statti "Debtorska zaborgovannost for vidanimi advances" to show the sum of advance payments, giving to the receivers in the races of offensive payments.

30. The stati "Debtorska zaborgovannost z nahahovinyh prodaziv" shows a sum of nasokhovanih diviendendyv, interestiv, royalty tochno, scho pidlyagayut nadohodzhennyu.

31. At statti "Debtorska zaborgovannost iz vnutrishnih rozraunkiv" show the fence of the people who stay in the city and who are deported from the country in the first place.

32. At statti "Інша it is flowing дебіторська заборгованість" it is shown заборгованість дебіторів, яка can not be included until the latest articles дебіторської заборгованості я яка відображається у складі оборотних активів.

33. At statti "Поточні фінансові інвестиції" vіdobrazhayutsya fіnansovі іnvestitsії on lines, but I do not transfer one рік, які мууть бути вільно реалізовані at any time (крім інвестицій, які є еквівалентантами грошових коштів).

34. In stati "Grošivi koshti ta ekvіvalіnti" vіdobrazhayutsya кошти в касі, on the current and other rahunks at banks, yakі mozhut bouti vikoristani for current operations, and takozh ekvіvalіnti groshovih koshtіv. At the same time, it is possible to be introduced into the national currency and in foreign currencies. Кошти, які not possible використати for operation with the extension of one rock починаючи з дати balance with the extension of the operational cycle внаслідок обмежень, слід виклюти зі warehouse of the turnaround activists and vіdobrazhati yak neoborotnya activa.

35. In statti "Інші оборотні активи" vіdobrazhayutsya суми оборотних активів, які can not bouti included until the guidance of the articles is rozdilu "turnaround activists."

36. In statti "Vitraty maybutnih periodiv" vіdobrazhayutsya vitraty, scho mali mіsce through the flow of abdominal transient zvіtnih periodov, ale nalezhat up to the coming zvіtnih period.

37. Stati "Statutniy kapital" is imposed in the installation documents zagalnaya vartit active, yakі є vneskom vlasnikiv (uchasnikіv) to kapitalu pіdpriєmstva.

38. In statti "Payovyi kapital" it is necessary to induce a sum of money for the members of the spouses of those other pensions, but it is peddled with the set documents.

39. In statti "Dodatkovyi kapitali kapital" associate partnerships show the sum, on the yak vartizst realizatsii vipuschenih ackіy perevishchu Ёх nomіnalnu vartіst.

40. The stati "The most dodatkovy capitals" vіdobrazhayutsya suma to otsnki neoborotnyh active, vartit active, bezkoshtovno otrimanih pidpriemstvom vid іnshih juridicheskikh obsoznyh osib, taіnshі vid dodatkovogo kapitalu.

41. In stati "Reserve capital", a sum of reserves shall be imposed, wagering up to the proper legislation, installation of documents for a raunch of unfinished pidpitem pidpriemstva.

42. In statti "Nerozpodoleny pributok (nepokrytiy zbitok)" vіdobrazhaetsya abo suma pribudku, yaka reinvestvana at pidpriemstvo, abo sumo nekritogo zbitku. Suma nepokritogo zbitku induce in the arms and virahovuyutsya with viznachennі pidssumku vladnogo kapitalu.

43. At statti "Neoplachenie kapital" vіdobrazhaєtsya suma заборгованості власників (учасників) behind extracurricular activities to the statutory capitals. The sum to be invested in arches and virahovuyutsya at viznachennі pidssumu vladnogo kapitalu.

44. In statti "Visuleniy kapital" the gospodar's comrades vizobrazhayut actual sobivartіst іtcіy vіsnoї іmіііії abacus, vypupleny comradeship yogo uchasnikіv. Sum of the Vilnius capitallu is induced in the arches і підлягає вирахуванню at the sighted pіsumku of the imperious capital.

45. At the warehouse, the advance payment of the vitrate and the payment is to be accrued in the accrual of the transfer of the Maybutni vitrati that payment (the vitrati for the payment of the Maybutny Islands, the guarantor of the zobov), the amount of which on the storage date the balance may be indicated by the hat of the forward (predictive) Takozh shots koshtiv tsіlового фінансування і цільових надходжень, які отримані з бюджету та інших джерел.

46. In statti "Dovgostrokovi krediti bankiiv" show suman zaborgovanosti pіdpriєmstva banks for otrimaniem vid them poskami, yaka not є posochnym zobov'yaznyam.

47. In statti "Інші довгострокові фінансові зобов'яяня" it is possible to induce a sum of dovgostrokovoї zaborgovanosti підприємства schodo zobov'yаnya із залучення позикових коштів (крім creditів банків), на які доховуться відсотки.

48. At statti "Відстрочені податкиі зобов'язання" it is shown сума податків на прибуток, що підлягають сплаті в майбутніх періодах внаслідок тимчасової різниці між обліковою та податковою база оцінки.

49. In statti "Інші довгострокові збов'яяня" it is shown сума довгострострох зобов'язань, які can not be included in up to the next articles "Родівців".

50. At statti "Korotkostrokovi krediti banki" vіdobryazhyаtsya sumochnykh zobov'azan pіdpriєmstva before the banks for otrimaniem vіd them poses.

51. At statti "Post-zaborgovannost for dovgostrokovymi zobov'yazannami" show suma dovgostrokovyh zobov'azan ', yaka pіdlyagayє paused in the course of two months of the date to the balance.

52. In the "Vekselі Vidanі" ("Vekselі Vidanі"), a sum of zaborgovanosti is shown, yaku pіdprієmstvo saw a vіelіsі to the supply of supplies (robot, іsg) of bailiffs, підрядчиків та інших кредиторів.

53. At statti "Creditor's fence for a comrade, robot, ambassadors" to show the sum of the fines for the post-ies and pidrjadchikam for the material values, the vikonan roboti otrimanyi obggi (krim zaborgovanosti, breezed bills).

54. At statti "Potoknі zobov'yаnya za priadni аванimi advance" vіdobražaєtsya suma advance, vіdnіchіy vіd інших осіб у рахунок наступних поставки продукції, виконання робіт (послуг).

55. At statti "Potoknі zobov'yаnya із rozraunkіv z budzhdetom" it is shown the fence of payment for all types of payments to the budget, including the contributions from the administration of receivables.

56. In statti "Potoknі zobov'yаznya z pozubudzhetnih zapresіvі" it is shown заборгованість for extracurriculars to pozabudzhetnih fondіv, peredbacheny by chinnim legislation.

57. At statti "Potoknі zobov'yаnya zі strahuvannya" відображається сума заборговаіні за відрахуваннями до пенсійного фонду, на соціальне страхування, страхування майна підприємства та індивідуальне страхування його працівників.

58. At statti "Potoknі zobov'yаnya za rozraunkami s zasasnikami" vіdobrazhaєtsya zaborgovіnost pіdpriєmstva yogo uchasnikam (zasnovnikam), povyazyana z rozpodilom pributku (dividendi tochno) and the formulations of the statutory capitals.

59. At statti "Potoknі zobov'yаnya із intіrіshіnі rozraunkіv" vіdobrazhayutsya zaborgovannі pіdpriєmstva povdjazanim sides that the creditor's zaborgovannі z z vіtrіshynovіdichih rozraunkіv.

60. In statti "Інші поточні зобов'язання" відбражаються суми зобов'язань, які can not bouti included in the up-to-the-minute articles, navedenih at rozdіlі "Поточні зобов'язання".

61. Up to the warehouse of income, the Maybutnykh periods are included in the income, by the extension of the flowing transaction of the cross-checking periods, until the upcoming zvіtnih periodov.

Оцінка та розкриття articles balance

62. Otsіnka that is further away from the back of the articles to the balance sheet in the notes to the public in accordance with the requirements (standards) of the accounting region.

Head of the Management of the Methodology of the Accounting Sector of the Ministry of Finance of Ukraine V. Parkhomenko

Dodatok to Poslozhnya (standard) of the accounting region 2

Balance at _ 20_r.

Form number 1 Code for the VKUD | 1801001 |

| Assets |

Code Row |

On the ear of the zvitnogo periodu |

At the peak of the translation |

1 |

2 |

3 |

4 |

І. Non-reversible activation |

|||

Unmetered Activation: |

|||

Zalishkov vartism |

010 |

||

Первісна вартість |

011 |

||

Abrasion |

012 |

||

Незавершене будівництво |

020 |

||

The main problems are: |

|||

Zalishkov vartism |

030 |

||

Первісна вартість |

031 |

||

Abrasion |

032 |

||

|

Довгострокові фінансові інвестиції: To be used for the method of participation in the capitalization of in-kind facilities |

040 |

||

Інші фінансові інвестиції |

045 |

||

Довгострокова дебіторська заборгованість |

050 |

||

Submitting a credit report |

060 |

||

Інші необоротні activator |

070 |

||

Immediately after the birth of I |

080 |

||

1 |

2 |

3 |

4 |

II. Revolving activates |

|||

Stock up: |

|||

Vibronichi stock |

100 |

||

Tvarini on virochuvanni ta vіdodіvіlі |

110 |

||

Uncompleted vibro |

120 |

||

Ready products |

130 |

||

Comrade |

140 |

||

Vekselі susteni |

150 |

||

Дебіторська заборгованість for a friend, robot, service: |

|||

Clean real estate |

160 |

||

Первісна вартість |

161 |

||

Reserve sumnovnyh borgiv |

162 |

||

Debitsorska zaborgovannost for rozraunkami: with the budget |

170 |

||

Behind visible advances |

180 |

||

From accrued income |

190 |

||

Із внутрішніх рахунків |

200 |

||

Інша поточна дебіторська заборгованість |

210 |

||

Поточні фінансові інвестиції |

220 |

||

Грошові кошти та їх еквіваленти: |

|||

At national currency |

230 |

||

In foreign currencies |

240 |

||

Інші оборотні activator |

250 |

||

Immediately after the birth of II |

260 |

||

III. Vitrati maybutnih periods |

270 |

||

Balance |

280 |

||

Passive |

Row Code |

On the ear of the zvitnogo periodu |

At the peak of the translation |

1 |

2 |

3 |

4 |

I. Vlasny kapital |

|||

Statutory capital |

300 |

||

Паявий капітал |

310 |

||

Додатковий вкладыли капітал |

320 |

||

Інший додатковий капітал |

330 |

||

Reserve capital |

340 |

||

Nerozpodileny pributok (nepokratii zbitok) |

350 |

||

1 |

2 |

3 |

4 |

Neoplacations capitals |

360 |

||

Blessings |

370 |

||

Immediately after the birth of I |

380 |

||

II. Payback of the onset of vitrage and payments |

|||

Payment of benefits to staff |

400 |

||

Інші забезпечення |

410 |

||

Цільове фінансування |

420 |

||

Immediately after the birth of II |

430 |

||

III. Довгострокові збов'язання |

|||

Довгострокові кредити банків |

440 |

||

Інші довгострокові фінансові зобов'язання |

450 |

||

Відстрочені податаі зобов'язання |

460 |

||

Інші довгострокові збов'язання |

470 |

||

Immediately after the release of III |

480 |

||

IV. Potochny zobov'yana |

|||

Короткострокові кредити банків |

500 |

||

Поточна заборгованість за довгостроковими зобов'язаннями |

510 |

||

Векселі видані |

520 |

||

Кредиторська заборгованість за товари, роботи, послуги |

530 |

||

Поточні зобов'язання за розрахунками |

|||

з одержаних авансів |

540 |

||

з бюджетом |

550 |

||

з позабюджетних платежів |

560 |

||

зі страхування |

570 |

||

з оплати праці |

580 |

||

з учасниками |

590 |

||

із внутрішніх розрахунків |

600 |

||

Інші поточні зобов'язання |

610 |

||

Разом за розділом IV |

620 |

||

V. Доходи майбутніх періодів |

630 |

||

Balance |

Kerivnik

Головний бухгалтер_

Comments

When commenting on, remember that the content and tone of your message can hurt the feelings of real people, show respect and tolerance to your interlocutors even if you do not share their opinion, your behavior in the conditions of freedom of expression and anonymity provided by the Internet, changes Not only virtual, but also the real world. All comments are hidden from the index, spam is controlled.