| home

|

Фінанси (теоретичні bases) - Грідчіна М.В.

Розділ 7. Financial control

7.1. Suitability and visibility of financial control

Підвищенню ефективності функціонування фінансової системи та її складових сприяє фінансовий контроль.

Z one boku , financial control є okremim type of zagalnіy sistemy control, sho hoplyuєe admіnіstrivniy, pravoviy, tehnichny, ekologicheskii ta іnshі spetializovanny ty control. On the other side, financial control is a special kind of managerial activity in the sphere of economical know-how, which is imposed on the citizens of the government processes and operations, the lawfulness, the provision of property, the state property, the safe keeping of the koshtis.

The objective basis of financial control is the control function of finances, the organ is organically attached to it, the management of the management is responsible for shaping, rozpodilom and vicarities of the gross suppository product.

Sutnіst fіnansovogo polyagaє control in integrated, organіchno vzaєmopov'yazanomu vivchennі zakonnostі gospodarskih i fіnansovih operatsіy i protsesіv on osnovі vikoristannya fіnansovoї zvіtnostі, buhgalterskogo oblіku, normativnoї that іnshoї ekonomіchnoї Informácie in poєdnannі s doslіdzhennyam factuality will ob'єktіv control s metoyu zabezpechennya efektivnosti vikoristannya fіnansovih resursіv .

The subject of financial control роз rozpodilnyi pererozpodilnyi process in the form of vikoristan financial resources in all regions of the economy of the territory. Up to the sphere of financial control, it is practical to use all the operations that are caused by the ruin of the sovereign's koshtiv and the gospodarstvo diyalnisty, that in the economical literature is often used the term "financial-gospodar control".

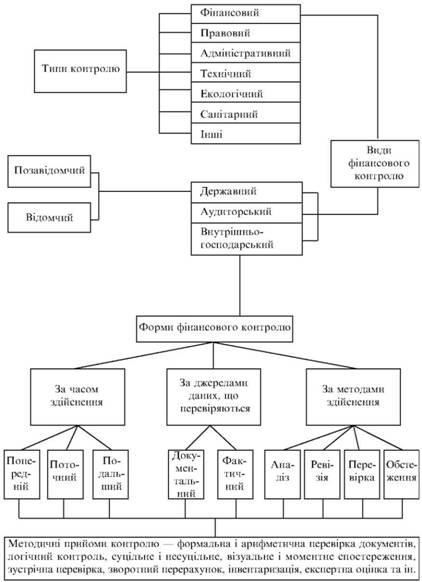

Розрізняють такі види фінансового to supervision: державний, аудиторський та внутрішньогосподарський. To see the financial control of the forms, they can be identified with the singing marks. So, for an hour zdіysnennya viokremljuyut transient, current and submissive control; For the gems of the tributes, but for re-negotiating, - documentary and factual; For the methods of vikonannya - revizii (complex nepokleksnu), perevirku, analiz and obstezhennya (Figure 7.1).

Fig. 7.1. Classification of financial control over types, types and forms

The forward control is the form of the financial management of the state, a kind of zdіysnjєyatsya to the back of the gospodarskih operatsiy. Until then, all the organisms are collected, and the control functions are vikonuyut. Чітка оргаізація обліку і and cross-check control сприяє запобіганню зловживанням у використанні коштів, товарно-матеріальних цінностей.

Potokniy (operative) control, which is the implementation of the operations of the Lord's Gentlemen, it is against the vyachasnym viyavlennju vidhilen at the financial-gospodskiy diyalnosty pidrkontrolnogo obekta.

Submitted control (control over the fact) здійснють після годарських операцій. For dopomogo this control vyyavlyayut illegally vikonannya gospodarskih operatsi, and takozh vinnih u ts'omu. Meta control over the fact - vidshkoduvati zbitki, attract vinnyh before vidpіdalnosti, create umovi, scho uemozmolivyatimut reiterated zlozhivan.

Documentary control means, scho perevіryaetsya достовірність, правоність та господарська необхідність годарських операцій на підставі документаів, у яких вони відображені. Control of the work of the document and document; With the help of dostrichnyh perevirok dostovirnosti accounting operations, zafiksovanyh documents; Interdisciplinary control of operations and documents; Analitichnimi and logistic priyomyami.

The actual control of the field is in the actual conversion of the assets, the main assets, commodity-material values, rozraunkiv, їх відповідності given to the accounting area.

Фінансовий контроль як спеціалізований kind of management of the economy of the economy. Galuz ekonomichnyh znan znanabacha zastosuvannya riznomanitnykh metodicheskikh priyomіv (sostiv), yaki basyayutsya na dosyagnenney sumyhhnyh sciences (analiza godarskoi diyalnosti, accounting region, statistican іn.). Systematize in obrobicnyh reach the kombinovaniem vikoristannyam riznyh methodical priyomіv documentary and actual control (Table 7.1). Їх застосування дає змогу всебічно аналізуваі і синтезувати фактичний матеріал, з'ясувати послідовність дій суб'єкта control of the folding gospodarskih situations, abo in the minds of unrecognized, vstanoviti dostovіrnіst zaruchteni dzherel інформації.

Dzherelami information for documentary control є pervinni documentation; Реєстри бухгалтерського обліку; Data of the operational and technical area; Form zvіtnostі, planova, normativna, proektno-

Table 7.1

Methodological documentation and actual control [33]

| Documentary control | Actual control |

|

Formal and arithmetical translation of documents Legal assessment of the image In the documents of gospodar's operations Logistical control of the objectivity of documentary registration of gospodar's operations Sutsіlne sposasteryzhennia Nesucilne (at that number vibrique) Zuestichna perevirka documentів або записів в облікових реєстрах Zorotniy rosyraunkok Оцінка правоності й обґрунтованості годарських операцій за даними кореспонденції рахунків бухгалтерського обліку Balansov porivnyannya ruhu commodity-material tsinnostey Portivnyanya, grupuvannya, rozraunkki Середніх і відносних показників Ta інші прийоми економічного аналізу |

Inventory Експертна оцінка справжніх обігівіві and anchorі виконання робіт, обґрунтоності нормативів матеріальних витрат і виходу готової продукції, дотримання технологічних режимів (viznachennya vіkonanii robіt, checking the launch of syrovini and materіalіv in vibrobnitsu, laboratory analiza) Візуальне спостерження - безпосереднє обстеження і огляд складських приміщень, цехів Momentno sposberezhennia - timekeeping, photografiyya robochogo day, інші дії for fіksatsії okremih elektіvі vibrohnicho-gospodarkih protsіvі pevnij perіiod |

Konstruktorska ta інша документальна інформація. Documents pereviryayut for the shape and zmistom. Otsіnemichi dokumentalnya dokumentv, slіd vyavlyati pravilnіst zapovnennya vsekh rekvizitіv dokumenty, nayavnіst neobumovleny vipravleny, pidchishchen, additions text і digits, vidpovdnist pidpisіv posadovyh i materіalno vidpіdalnih osib. In the case of the consumer, write the individual in the document and post it in a pie in the other documents, and then make the summons, return the individual to the individual, and get to the law enforcement agencies for the special expertise. Перевірка документаів за змістом полягає у критичній оцінці змісту документа.

Перевіряючи правоність і доцільність годарських операцій, що відображені in the initial documents, neobhіdno z'yasuvati, chi not to enforce its lawful legislation and normative acts.

In the case of unlawful gospodarskih operations, the controller is installed, for the sake of rozporyadzhennyam stinks zdіysnenni, and takozh rozmіr materialovnyh zbitkiv.

Достаірність годарських операцій, відображених at the first documents, у разі consumer can vstanoviti with the help of dzhestrenichnyh perevyrok on pidpriemstvah, in the institutions and organizations, z yakimi obekt, scho revizuyutsya zdіysnyuvav gospodarskie operatsi.

At zostrіchnih perevіrkah pervinnyi dokumenti і oblіkovі dіnі pіdpriєmstva porіvnjutsya з відповідними making documents and giving the organізацій, від яких вони отримані або якимким видані кошти і матеріальні цінності.

Wikis to the bank for the various users of property in various times, to be consumed in written records on the cih rahunks in bank establishments. Copies of paid documents, copies of documents, copies of the original documents, documents of the bank.

Vseemniy control of the operation of analogous documents, ali at the time of documenting the documents, they were invoiced in the form of one and the same pidpriemstva. Analitichnyi logisticny priyomi perebachayut vikoristanny rozraunkovyh, obsochlyuvvalnyh, log ychnih procedures for the documented documents. Наприклад, під час арифметичної перевірки viznachaetsya correctnost rozraunkіv for documents, for paid vіdomosti for vyplatu zabobitnії plati, vіdobrazhenijah kasovikh zvіtakh, підсумків та ін.

There are three ways to control documents: social, non-existent, and combinational. At sutsіlnogo sobiі perevіryayut usi dokumenty, povyazhany z oproktsiy, scho pereviryayutsya, nesotsilno-mu-lishe part of spetsialno vidnybranyh dokumentov. Combinations sposib means, scho part dokumentov pereviryayatsya sutsіlnim way, and part - nesotsilnim.

Існують такі види фінансово-господарської діяльності, грушення в яких найімовірніші. At such times, documents are re-interpreted in a suicidal way. Napriklad, tse opytії z rushom koshtiv u kasі, pidzvіtnih osib, rahunkah at the bank, expensive metalov, іnshih especily tsіnnih speeches. Nesuchitsilny control characteristics for reviziї regional records and initial documents at various times of the year, the Masovian Gospodar operations (the ruchu of commodity-material values, naraukhuvannya zabobitnoyi paysnі tnіn.). Same in such a situation is important - і підхід до вибірки і відбору первинних докуів. Науково обґрунтований відбір документаів і облікових записів підвищує ймовірність виявлення порушень і недоліків, скорочує термін ревізій, знижує трудомісткість їх проведення. Наукові підходи до відбору документаів виробляються на основі аналізу і узагальнення given the revizіynії practice. Analyz svidchit, scho z dvoh varyanti nesotsilnogo sposterezhenny at revizii massov gospodarskikh operatsy (perevyrki partni dokumentov for all mіsyatsі periodu, yaki rivizuyutsya, abo perivirki vseh dokumentov for kіlka mіsyatsіv) доцільніший перший варіант.

In practice, control and revising robotics, two variants of documentary information: from the first documents to the registers of the analytical and synthetic regions; Від звітних, підсумкових показників до реєстрів синтетичного і аналітичного обліку і Від записів у них - до первинних документаів. The other version of the rationale, the secrets of the past and the future, the basics of the analysis of the past, the present, the material, the literature, the documents, the documents, the documents, the documents, and the documents. A tse daє mozhnivіst zmenshiti kіlkіst dokumentov, scho perevіryayutsya, і termіni held revizii.

At different levels, the installation, the organisation and the registration of the combinations of the pidhid - the social control of the kasovih and the banking operations and the non-documentary control of the documents that are involved in the gospodarnye operations.

The actual control of the perebacha vivchenna spovojnogo stanu ob'ekta, scho perevyryaetsya, for material yoglyad yogo in nature. For the specialty of special registers in the actual control, in the event that consumers install the documents of the first documents and regional records. Іноді for paperlessly issued documents і write down крикуться розкрадання та інші зловживання. Methodical priyomi actual control is to mute at meti vstanoviti real mill, oaths and yakist vikonannya robot, spravzhnen zdіysnennya gospodarskih operatsi, scho vidobrazheni in documents.

Documentary and actual control is one to one, then to the subjoining on the priory. Napriklad, Inventory of commodity-material values, control, vimiriannya vikonannya robit obovvjazkovo otvoyazyakovo otvushetsya poryvnyannyam actual danykh z oblikovichi. Zustrіchna perevirka documentary giving of the supplier and order of commodity-material tsennosty often to be transferred to the actual fact of the natures in the warehouse for oderzhuvacha.

The main method of podalshogo fіnansovo-gospodarskogo control є revizііya. Vona ґruntuyutsya perevіrtsі bibliiskogoї і statisticheskogo zvіtnostі, pervinnikh documentov, oblіkovikh reekstrіv, factoї nayavnostі koshtіv і commodity-material tsіnnost. In the Law of Ukraine "On the Control of the Revival Service in Ukraine" [13], the method of documentary control over the financial and government dyalnіstyu pіdpriєmstva, establish, organizatsii, doktrimnyam legislativstva z fіnansovyh pitan ', достоірністю обліку і звітності, спосіб documentary розкриття недостач, розкрадань , Privlasnennya koshtiv і materialnichnih tsinnost, zabibannya fenansovim zlozhivannyam.

Перевірка - це обвеження і вивчення окремих ділянок фінансово-господарської діяльності підприємства, establish, organizізації або їх підрозділів.

For the results of the revision, an act is to be deposited, and the results of the revision are to be drawn up in the form of a supplementary note on the vikonan robot.

Visnovki revizii obruntuyutsya documentary dostovirnimi evidence. Materialistu і juridnu vіdpovіdalіst for vyavleni pravoshennia to carry concrete osobi. Вони встанолюють також розмір exact збитків від втрат, недостач, розкрадань матеріальних цінностей і обґрунтовують виявлені системою докази (initial documents, vідомості івенвентаризації, explanatory notes матеріально відповідальних осіб та ін.). The most important step is the control of the robotics, the development of the programs of revision, the de-identification of the revolution, the meta ta basic pittany, on yakih slides of zosrediti respect. On the basis of the programs, a warehouse plan is made for carrying out revisions (relocation) for specific purposes of wards, periodu pereviroki, vikonavtsiv and terminov vikonannya revizii.

Залежно від змісту програми ревізії поділяються на повні (комплексні) і невні (непоплексні). Повні (комплексні) ревізії охотлюють усю діяльність об'єкта supervising the prom promіzhok hour. The criterion of complexity in the field of nasampered in the interdisciplinary control of technical, labor, organizational and financial-economic indicators, systemic economic policies (establish, organi- zation).

Comprehensive revisions are determined by the method of control, oskilki perebachayut vsebichnu perevirku vibronichego i fіnansovo-gospodskoї діяльності суб'єкта госдарювання ревізійною групою кваліфікованих фахівців різного профілю. Комплексні ревізії здійснють Рахункова палата, Контрольно-ревізійна служба, відомчі контрольно-ревізійні підрозділи, а також слідчі organization.

Непоні (некомплексні) ревізії охотнолюють one's abacus of stresses on the control of the control (on the application, vibrobitztvo, zbut, postachannya), okremі see operatsi (kasovi, rozraunkovi tochno), zberezhennya i rulednosti vikoristana rіznih vidіv zasobіv (basic zasobіv, goods, grosche тощо ). Nepovnyi revizii zdebolshogo zdіysnemuyut podatkovi, mitnі organii, Antimonopolitan komitet Ukrayiny, інші державні organization in the interiors of the competence behind these strains, which interfere with the right to control, and which organizes internal control, recognized as the keeper of enforcement (establish, organizatsii).

Vazhlivim і foldable є law vragulyuvannya і practical zastosuvannya legal norms shodo zahistu komercitsynoi taemnitsi pіdpriemstv in the process of financial control. Поняття "комерційна таємниця" встановлене The Law of Ukraine "About pідприємства в Україні" [20]: tse vіdomosty, povysheny z vibrobnitsvom, tehnologіchnuyu informatie, management, fіnansami thіnіshimi pomіmkіmі діяльності підприємства, що not є the state taєmnіyu, rozgoloshennya (переданняня, поширення ) Which can be used to gain access to the interests of enforcement. The main document, which is viznachaet order і umovi organizatsii uzhorni komercinoy taemnitsi na pidpriemstvі, є kazhivnik's order on pidstavi ch. 2 tbsp. 30 to the law, it is designated, but the warehouse and the voucher of visas, to become a commercial taemnitsu, order їх захисту визначає керівник підприємства. Відомості, які не бууть бути комерційною таємницею, встанолюються постановою Кабінету Міністрів України "About перелік виімомостей, що не складають комерційну таємницю" № 611 onі 09.08.93. Zgіdno z tsієyu decree komercynyu taєmnitsu not to install the documents, and so tako, scho allow to borrow pidpriemnitskoy ne gospodarskoyu diyalnistyu; Information in the course of the restoration of forms of state control; Danis, neobhіdnі for perevirki naryakhuvannya і спла спла та та та та та та; Відомості about чисельність і warehouse of pratsyuyuchih, їhnyu zarobіtnu fee zagalom і for professiami ta posadami, pro nayavnіst vіlnih robočih mіts; Documents on the finality of payments and obovyazykovy payments; Information about zabrudnnya nakkolishnogo sredovischa, nedotrimannya bespechchnykh minds pratsi, realizatsii production, scho zavedaetsya schody zdorovju, and takozh about inshi pograshannya legislativnosti Ukrainі і розміри збитків від; Documents about platosprodmonnost; Відомості about the fate of posadovyh osіb підприємства в інших оргаізаціях, що займаються підприємницькою діяльністю; Відомості, які підлягають голошенню згідно зчинним законодавством.

Pідприємства збов'язані надавати зазначені відомості authorities vіnavnochoї vladi, and takozh kontroljuchim і zakonohoronnym bodies. Згідно із Законом України "Про аудиторську діяльність" [3] відкриття бухгалтерської звітності, що становить комерційну таємницю, для проведення аудиту і надання інших аудиторських послуг, здійснюється користувачами бухгалтерської звітності. Іншими словами, законодавство забезпечує доступ до переважної більшості документів, необхідних для здійснення фінансового контролю, але водночас захищає підприємства від шкоди, яка може бути завдана розголошенням комерційної таємниці та конфіденційної інформації. Аналіз свідчить, що майже тридцять законів України мають окремі положення щодо захисту комерційної таємниці.

Наприклад, законами України "Про державну податкову службу в Україні" і "Про Державну контрольно-ревізійну службу в Україні" [13] передбачено, що їхні працівники зобов'язані зберігати комерційну і службову таємницю; у Кримінальному кодексі України за навмисне розголошення комерційної таємниці передбачено покарання позбавленням волі на термін до двох років.

Comments

When commenting on, remember that the content and tone of your message can hurt the feelings of real people, show respect and tolerance to your interlocutors even if you do not share their opinion, your behavior in the conditions of freedom of expression and anonymity provided by the Internet, changes Not only virtual, but also the real world. All comments are hidden from the index, spam is controlled.