| home

|

Podatkova polity - Litvinenko Ya.V.

4.2. Favors, õх functції та ви

Submissions є partly zagalnoy fіnansovoї sistemi yak power in tilomu, and і okremih її sub'єktіv. In addition, stink vidupayut odnієyu kategrіy rinkovoї ekonomiki.

Submissions of information in the sphere of vibrobnichi vidosnon, oskilki ви viluchennyam part vyroblenogo product (in groshovіy formi) in dohіd power. Ale of a present is a set of categories. Wants postynno zminuyutsya. Змінна й sphere їх дії.

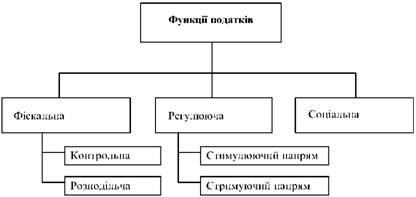

Sutnist podatkiv , yak ekonomichnoi kategori, manifested through the functions, yaki vony vikonuyut. Look at the three main functions of the submitter (Figure 25).

Fiscal function . Її сутність полягає в забезпеченні надходження коштів до державного бюджету. In the be-yak suspilstva

Fig. 25. Functions of submissions

The function is to be implemented. For її dostomoyu vidbuvayetsya formovaniya fіnansovyh resources of the state, the recognition for pokrtya vitrat, povyazyannyh іz vikonannyaem svoїh its functions - ekonomichnyh, sotsialnih, oboronnyh, zharoni zdorovya, ekologicchnyh tochno.

Do your chergo, tsya functitsіya podіlyaetsya on dvі (vykakі ekonomisti vchenі vidіlyayuyut їх okremo): I control that rozpodilchu.

Control function . Vona polagayє in the obliku kіlkostі podatkіv і rozmіru kozhnogo z them, and takozh in otsіntsi efektivnosti dermal canal nadohodzhennya podatkiv. Tse perebachaet not tilki zdіysnennja to the control for otrymannyam submissions, and throughening of rare sanktsі to pravoshnikiv. In addition, the vikonannya tsієї functіії peredachaє takozh voznesennya postійних змін beside the system оподаткування з метю підвищення її ефективності, яка зажить від ісуючої in the power of the taxable disciplinary, the lawfulness of paying the taxes to the state before the power. Basically meta tiєї functiії - досягнення своєчасної і повної за обгаг ordering.

Виконання розподільчої функції по'язане зі стягненням податків і забезпеченням наповлнення бюджету, який потім буде розподілений. At vikonannі tsієї functіії the power is guilty збирати постійні, стабільні та рівномірні податки.

Postinism in otrimanni podatkiv means, scho voni povinni podhoditi to the budget not in vyglyadі razvivh payments, and the extension of the budgetary budget in a few lines in a row with zynnim legislation.

Stability is signified, and the duty of submission is guilty of vysnachatis vysokim rivnem garantiії of that, podobacheni by chinnim legislativnom submissions of the power otrimae at the pervasive obyazi.

Рівномірність means, пo submissions повинні розподілятися on території with such a rank, you can safely reach all budget forms in the state and on the river.

Regulyuyucha funktsiia . Її сутність полягає в перерозподілі вартості валового національного продукту між державою та планиками податків. Fidelies with the use of utomlyuyut osoblyvі mehanizmi, yakі zabezpechuyut balance of individualities and gagalnoderzhavnih interests.

Meta tsієї functіії - забезпечення неперерырніні інвестиційних процесів, зростання фінансових результатів бізнесу, сприяння збільшенню коштів.

Виконання регулюючої функції передбачає:

1. Viznachennya sistemi obodotkatvannya. Alya system of obodotkatvannya guilty postyno pristosovuvatis to osoblivostey rozvitku ekonomiki powers, situatsy, yaki zagalis, planovnih reforms tochno. It is not important to formulate this important thing, but to adopt the system of obedotkuvannya, zmіyna існуючих податків, methodology їх розрахунку, плоти тощо.

2. Efektivnist zastosuvannya podatkіv zalizhit vid їх progressivnostі, mozhnostyі otrymanny be-yakih пільг і zagalnogo zmenshennya in the interstices of legal legislation. For dopomogo podatkovyh pіlg power mе zmіgu reguljuvaty konjjukturu zagalnostrovnogo rinku kіlockів і послуг. Povstovlennya podlkovyh pіlg daє mozhnivіist pіdpriєmstvu zbіlshity its own дохоходи, прибуток, знизити витрати та ціну виробу, збільшити реалізацію продукції. І навпаки, збільшення розмірів in the field of the taxation to bring up to the payment of the price that zmenshenya obshygіv виробництва.

3. Viznachennya podatkovkiv rates. The power to install the rates of assistance and to differentiate it from the system to the system of economic development. Differential treatment is conducted in the form of pidpriemstva, that is, the form of yogo vlasnosti, the directionality, the responsibilities of the vibrokittyva abo nadannya, the ambassador, the importance of yoga for spozhivachi and the power, and also the time of the subordination of the sub-ecotourism.

Slid zazchachiti, scho vikonannya tsієї functiії podatkіv podal'shim rozvitkom zinkovyh vidnosin guilty bouti gnuchkishim (for umovi, scho zagalna system obodotkuvannya zalishetsya nezminnuyu). So, vіd vikonannya regulyuyuchoi functiiі zalezhit rozvitok pіdpriєmstva, zatsіkavlenіst s roshyshrennyi obyagіv dіyalnі. A gift for a pributok viznachaet that yogo part, yaka zalishaetsya in rozporyadzhennyi pidpriemstva. Yakshtso a gift for a pributok enchantingly great, tse zmenshuyu zatsіkavlenost pіdpriemstva in yogo otrimanni, i vono namagaєtsya prihovati pributok і be it any zakobami zbіshshiti fund pay for money інші витрати або зменшити ширина діяльності. With zmenshenni podatku on pributok kci funktsi mozhe vplytiti on that part, yaka pідлягає капіталізації. Jaksho zloku power to be conducted polity, spymovana on stimuljuvannya kapitalovklokden (napriklad, nadayutsya pіlgi at інвестуванні у нові виробництва, придбанні обладнання та прискоренні його амортизації), then a part of the pributku vikorostvuyutsya on tsі tsіlі. Якщо держава зменшує або взагалі скасовує оподаткування дивідендів, then підприємство зацікавлене у збільшенні споживчої частини прибутку і підвищує розміри дивідендів на свої акції.

In mezhah vikonannya tsієї functіії vidilayut two її straight: stimuljuyuchy that strimyuchy.

Sutnist stimuljuyuchogo strained polyagaet in nadanni podatkovyh pіlg abo zvіlennіі vіd zaplati zapatkіv vzagali.

Strizmuyuchy strained to zasstosovetsya, if the power of bazha zahistiti vlasy vibrochnika. For the purpose of the installation of add-ons, the payments are to be made by the tariffs of the tariffs (for example, the excise duty on the mountain of the Tyutyunivi virobi in particular). At the result of the growth of the price of the virologic, I can not compete with it.

Yak nadannya пільг, so і різні стримуючі важелі застосовуться незалежно від вид підприємства, галузі виробництва чи обслуговування.

In Ukraine, the special meaning of Nabuva is the function of submissions - social. Ії виконання сутєво впливає на добробут громадян та справедливий розподіл коштів sovereign budget між усіма верствами населення.

Submissions to "feed for"? And in your life, on the first plan, you should see the supply of "for whom?". The payments are to be made for the oversupply of the state structures and for the protection of them by the functions of management, defense, social, economic and other. Wongs do not mute ni elements of a specific exchange of mercenaries, nor specific confession. So, with vidrahuvanni koshtiv on obovyazykov pensyne, the payer knows, if, in spite of the penny's wit, the stink of paying pensions. Tse stosuyutsya і obovvyazykovy payments on insurance for vipadok bezrobitsya, payments to the Innovation Fund of the інших відрахувань та платеів. If the money is distributed (for example, for pributok, pributkovy podatok z gromadyan, podatok on dodanu vartiz tushcho), then the payer does not know, on shcho budut vitracheni tsi koshti: on osvitu, zharonu zdorov'ya, on utriannya zbrroynih forces tochno. Ці кошти акмулюються в державному бюджеті, а потім розподіляються The Supreme Rado of Ukraine with the yogo затвердженні. This is a gift - not a legal matter, but an economic category. At stjagennnі that отриманні податку відбувається перерозподіл частини засобів власності усього суспільства. Otzhe, podatki vystupayut and ik form pererozpodilu natsionalnogo income. Інші обов'язкові paymentі відрахування, выски to the budget of the state †"presenting gifts for the form, not for the suttyu.

The gift is set by the power of the і і тільки її attribute. The payment of a contribution to the law and the form of manifestation of sovereign sovereignty. Індивідуальність a payment is shown in the fact that, under the yogo stagnant power, take on yourself obovvozyaki nadannya kozhnomu platniku viznachenogo ekvіvalena, yak dorivnyuatime rozmіr yogo payment.

The payments are to be contracted more than once, and periodichno, in the line, viznacheni chinnim legislation. Відносини, що складаються при визначенні розміру a payment of that yogo сплаті, to be regulated by the rules of the financial law, yakі in сукуності створююют the institute of the tax law. In addition, special rules are imposed, which are imposed on the dowry cut, the order of naryhau is reduced, the amount of payment is collected, the lines of the packing, the payment, the payment of the payer, the order of the oscar, and that of the fines. Submissions do not materit terriorialnogo zakriplenostі and do not lie until concrete warts of the payer.

Alya in the gifts of the pledged activities of superintendence. It is obligatory to pay a payment to the zmenshennya of the payspayer's penny-free income. In the course of their skinning, they zatsіkavleny at zmenshennyi basis otopototkuvannya, in order to change the mix of the feeder. On the other side, the power is encapsulated in otrimanni podatkіv in the pendent obyazi. That way, yak vikonuetsya fіskalna functіія, to lay a vidnoshennya pays the payment to the power. And in addition, yak vikonuetsya ekonomichna funktsiia, to deposit stavlennya power to payer tax.

Alya treba mati na uzizi, scho podatki not zavzhdi nahahovuyutsya z dikh dzherel, yakі viznachayutsya prinnym legislativstvo, tobto ob'ektat otpototkuvannya that sub'ekt, yak richer, you can not zbigatis. Platnik submitting a duty zavzhdi bazhay pereklasti plattek podatkіv na іnshih sub'єktіv rinku: на споживачів за рахунок підвищення ціни iѕ proportionalі zоstnіnu podatku nіt na tih, vіd otsimuє itself virіb, on taku sumu, yaka b dorіvnyuvala yogo varmostі for іmvі vіdsutnostі ціого подать визагалі. Do action vipadkah tse vidbuvaetsya in the national economy. That is the problem of the viznachennya spherical shift and іпливу кінцевих paragraphів, куди податок переміщується. The process of transfer is undermined by a number of submissions. Ces can rozgljanuti on these butts.

Оподаткування фізичних осіб. Styagnnnia pributkovogo podatku stosuyutsya vseh gromadyan Ukrainy, yakі povinni rlyuchuvatse tsei podatok і мають дохід, що підлягає, згідно з чинним законодавством, оподаткуванню. Yakshtso platnik podatku maє right self-instaluvatyvati tsіni na svіy virіb otb oglu, then you can transfer the amount of the payment to the settlers. For example, a loan, a loan, a loan, a private loan, a pick-up for a price, you can pick up money for your service in proportion to the amount of money you pay to the method of compensating for the citrate, and so you will pay a fee in the amount of one, one, one side, a positive moment for pricesses, And the other - zbіlshuє vitrati robotodavtsya і, відповідно, підвищує ціну виробу. Тобто підвищення заробітної плати працівникам means dodatkovu a mix of taxes (both through a pay-as-you-go, and with pribannі goods). Tse stosuyutsya і podatkiv in the fall.

A gift for pributok pіdpriєmstva. Sphere zastosuvannya that perelokdannya yyogo podatku dos dozhdena. Yakshcho pіdpriєmstvo vstavlyayuet tsіni, rozrahovoychi otrimati naiibilshy pributok, then, if you introduce a new payment, vozno mozhe і not pidvishchuvati tsinu chi zmenshuvati vyrobnitsva. At цьому разі співвідношення між цінами та отриманим the maximum прибутком bude is practical незінним як prior to entering, so і після entered the yyogo podatku. The entire sub-prime tyagar is lagging in the company's offices, in the presence of a mismatching rozmіru divвіддів abоmenshego rozmіru nerozpodіlennogo pributku. Ale company can transfer all of the rake of a new payment to the settlers, pidvishchichi tsinu on the holy virobes in a proportionately new payment. In addition, svyatkovy tyagar mozhe buty perekladenyi і on the post-urchin for rahunok kupіvlі resursіv for the lower price. Ale, as a rule, is a pererozpodil of the taxable draft of the taxable deposit to the estate of the landlords of the paperns (the transfer of shares) for the rajunks of the redistribution of divorces.

Excise zbir . The scope of the day is not very high. It is important for the platnik to recast the excisable excise tax on spozhivacha, napriklad, alcoholic drinks, confectionery vibrobs, and so on, the rest of the money can be bought from the virobi for the lower price, then the number of comradely virbitnitsva (abo alcohols at home vibrobit). Pіdvischennia tsіni mozhe nastilki zmenshiti vyrobnitvva, scho platnik zgoden budee tsi podatkovi vitrati take on yourself. Alye is here vinikayut rіznі varіanti. Наприклад: • збільшення ціни відбувається postup at small rozmіrah, tobto spozhivach postupovo zvikaє to the unknown pіdvischenya tsіni;

• The re-leasing of the platts is possible in quiet vipadkas, if there are companions in the ditch, and analogues of virobi should vydriznyayutsya for them for a yakistyu.

Otzhe, perekladannya excise zboru on spizhivachich vbdbuevaetsya nasampered through pіdischennya tsini.

A deposit on the lane, yak to be built for rent. In this case, the transfer of the payment is made through the payment of the rent payment, and the delivery of the levy is transferred to the bank account.

Tse stosuyutsya і zakonkikh інших податкових платеів.

Velike znachenny at doslisdzhennyi sistemi otapotkutvannya, vpivu vnutrishnih i zovnіshnіh chinnikіv, at rozbrotsi podatkovoї polity of the power of the country in the classics of submissions for riznyim znakami. Її необхідність viznachaєtsya різновидами податкових форма і застосуванням різних податковихі regimes. At tsyomu vrahovuyut soblivostі їх rozraunku, razlichi, vіdnesennya on vitraty vibronichego dіyalnostі tochno.

Перша знака - належність до рівня суб'єктів, які отримутть податкові платеі: залогондержавні та місцеві податки. Розподіл за цією знакою визначається згідно з Law of Ukraine "About the system оподаткування" since 25 червня 1991 р. №1251-12 in the editorship of the Law dated 18.02.97 р. No. 77/97-ВР with the advancements of those dopovnenni. (Dali submitted by the reimbursement of those who have received the obovyazkovyk payments to the Urakhuvanians, dopovnen ta zmіn.) The transfer of fiscally submitted taxes, the collection of those obovyazkovichi payments is filed in Art. 14 of the curse of the law:

1. The payment for dodanu vartist.

2. Excise duty.

3. A payment for a surplus of receipts.

4. A payment for the payment of fizichnih osib.

5. Mito.

6. The power of mito.

7. A gift on the non-farm mayno (nerukhomist).

8. Payment (payment) to the land.

9. Rent of payments.

10. Filing in the transport authorities for those own vehicles and vehicles.

11. Filing for the pardon.

12. Zbir on geologoozvduvalnі roboty, yakі vikonuyutsya for rahunok the state budget.

13. Zbir on spetsialnoe vichoristan of natural resources.

14. Zbir for zabrudnenya nakkolishnogo middle.

15. Zbir on obovyazykov social insurance.

16. Zbir on obovjazykov the state pensiyne is not insured.

17. Payment for the patent trade for the activities of the visibility of property rights.

18. Fisovanov sylskogospodarskiy a payment.

19. Zbir on the development of viticulture, sadivnitsva and hmelyarstva.

20. A third zbir, Io cope with the pass through the national cordon of Ukraine.

Перелік місцевих податків, зборів та обов'язкових платів визначається ст. 15 to the Law. Before them lie two favors:

1. Submission of advertisements.

2. A communal payment.

And takozh 14 місцевих зборів та обов'язкових платів:

1. The hotel zbir.

2. Zbir on parkuvannya motor transport.

3. Rinkovy zbir.

4. Zbir for a kind of warrant for an apartment.

5. Resort Zbir.

6. Zbir for the fate of the banks on the subway.

7. Збір за виграш у бігах на іподромі.

8. Збір з осіб, які take the fate of grі on totalizatorі on іподромі.

9. Збір for the right використання місцевої симвоіки.

10. Zbir for the right to hold teleconference.

11. Zbir for holding a real estate auction, competitive sale and lottery.

12. Zbir for the proprietary terriotiyeyu prikordonnih areas by road, scho straight for the cordon.

13. Zbir for vidachu dozvolu on rozmіschennya ob'ektiv torghivlі ta spheri sgig.

14. Збір з власників of dogs.

The other sign is the number of submissions, zborіv that obovyazykovyh payment in the tsіnі virobu abo sobigi. За цією знакою виділяють такі види: 1. Submissions, yakі to enter at собівартість:

• zbir on obovyazykov social insurance;

• zbir on obovjazykov svervevne pensiyne inshanya;

• zbir to the state innovation fund;

• payment for land;

• payment for trade patent for the activities of the visibility of the patent;

• a pod for a pomel;

• Fixings of the Siverskospodarsky tax;

• a payment for advertising;

• communal tax is not enough.

2. Filing, zobriy ovovyazykovy payment, yak rallying with the receipt of goods:

• a payment for the admission of goods;

• Submissions from transport authorities for those of the self-contained vehicles and vehicles;

• zbir for zabrudnenya nakkolishnogo sredovischa;

• the power of the mito is small.

3. Feeds that zbory, yaki enter before the price of the virobu:

• the payment for dodanu vartist;

• excise duty.

The third sign is the dzherela basin. For tієyu vnimayu vidilyayut podatki, zbori that obovyazykovі payment, yakі rally for rahunok:

• Individual income (a payment for the donation of phisical autumns);

• Income for sale (payment for dodanu vartist);

• the financial result of the disallowance (payments to the surplus);

• Witrite pidpriemstva (zbir on obovyazykov sotsialnne insurance that obovyazykov stvevne pensiyne inshanya).

The fourth sign is for the subject of obohatkuvannya (for podatkovoyu base):

• Resource;

• Rent;

• на споживання;

• майнові (на нерухомість).

П'ята ознака — за методом розрахунку ставок оподаткування:

• регресивні;

• пропорційні;

• прогресивні;

• лінійні;

• ступеневі.

Шоста ознака — за засобом вилучення:

• прямі — податок на прибуток підприємств, на землю, з власників транспортних засобів та інших самохідних машин і механізмів, на нерухоме майно (нерухомість);

• непрямі — податок на додану вартість, акцизний збір, мито.

Сьома ознака — за суб'єктами сплати:

а) юридичні особи — вони сплачують прямі, непрямі податки, збори в цільові фонди;

б) фізичні особи сплачують:

• прибутковий податок з громадян;

• податок на промисел;

• плату за землю;

• податок з власників транспортних засобів та інших самохідних машин і механізмів;

• мито;

• державне мито;

• внески (індивідуальні) на державне пенсійне страхування;

• внески на страхування на випадок безробіття;

• торговельний патент;

• єдиний податок (для тих фізичних осіб, які здійснюють підприємницьку діяльність за спрощеною формою сплати податку та бухгалтерського обліку);

• місцеві податки та збори.

Comments

When commenting on, remember that the content and tone of your message can hurt the feelings of real people, show respect and tolerance to your interlocutors even if you do not share their opinion, your behavior in the conditions of freedom of expression and anonymity provided by the Internet, changes Not only virtual, but also the real world. All comments are hidden from the index, spam is controlled.