| home

|

Finance and Statistics - Ковалева А.М.

6.8 SIMPLIFIED SYSTEM OF TAXATION OF SUBJECTS OF SMALL ENTERPRISE

At present, enterprises belonging to small business entities and individual entrepreneurs pay taxes either in accordance with generally established tax legislation or have the right to switch to a simplified taxation system in accordance with the Federal Law "On a simplified system of taxation, accounting and reporting for small businesses" From December 29, 1995 №222 ~ FZ.

However, not all small enterprises that are classified under the Federal Law "On State Support of Small Business" to small business entities can switch to a simplified system, but only organizations with a maximum number of employees (including those working under contractual agreements and other civil law contracts) to 15 people, provided that during the reporting year the aggregate amount of gross proceeds did not exceed a hundred-thousand-fold minimum wage.

Consider the main provisions of the current Federal Law of the Russian Federation "On a simplified system of taxation, accounting and reporting for small businesses." This system of taxation provides for the replacement of the payment of the aggregate of taxes established by the state by the payment of a single tax calculated on the basis of the results of the economic activity of the enterprise for the reporting period, although the current procedure for payment of customs duties, state duties, tax on the acquisition of vehicles, licensing fees remains for organizations applying this system , Deductions to state social extra-budgetary funds. Thus, it can not be said that a simplified taxation system is really a simplification.

The object of taxation is a single tax either the aggregate income of the enterprise or the gross revenue (at the discretion of the state authorities of the subject of the Russian Federation),

The aggregate income is calculated as the difference between the gross revenue and the value of the goods (works, services) used in the production process, the selling price of the property sold during the reporting period, and non-operating income.

The cost of raw materials, materials, components, purchased goods, fuel, operating costs, maintenance, costs of renting premises used for production and commercial activities, costs of renting vehicles are included in the cost of goods (works, services) used in the production process , Expenses for payment of interest for the use of credit resources of banks, services rendered, as well as VAT paid to suppliers, tax on the purchase of vehicles, deductions to state social extra-budgetary funds, customs fees paid, state duties and license fees. Single tax rates: no more than 20% of the aggregate income (10% to the federal budget) or no more than 10% of the gross proceeds (3.33% to the federal budget). Specific tax rates, as well as the proportions of the distribution of the enrollment of tax payments between budgets, are established by decisions of the state authority of the subject of the Russian Federation.

An official document certifying the right to apply a simplified taxation system by small business entities is a patent issued by the tax authorities for a period of one year. The cost of a patent is established taking into account the rates of the single tax by decisions of the state authority of the subject of the Russian Federation, depending on the type of activity. Payment of the annual cost of a patent is carried out by organizations and individual entrepreneurs quarterly. The paid annual value of the patent is credited to the federal budget, as well as to the budgets of the subjects of the Federation in relation to one to two.

For individual entrepreneurs, it is envisaged to replace the payment of income tax by paying the cost of a patent for engaging in this activity.

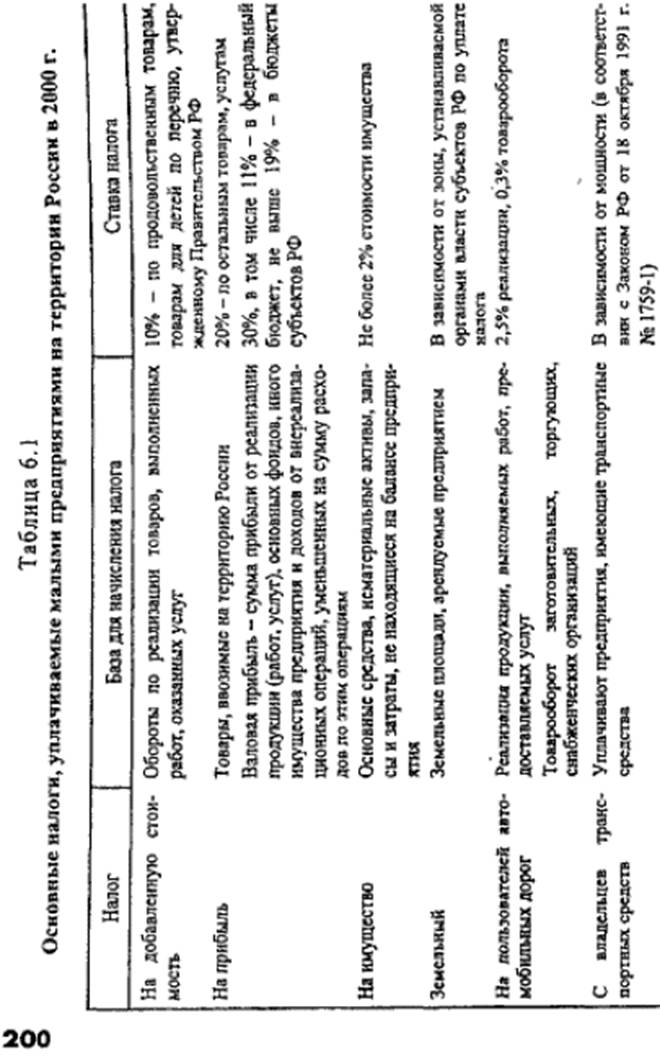

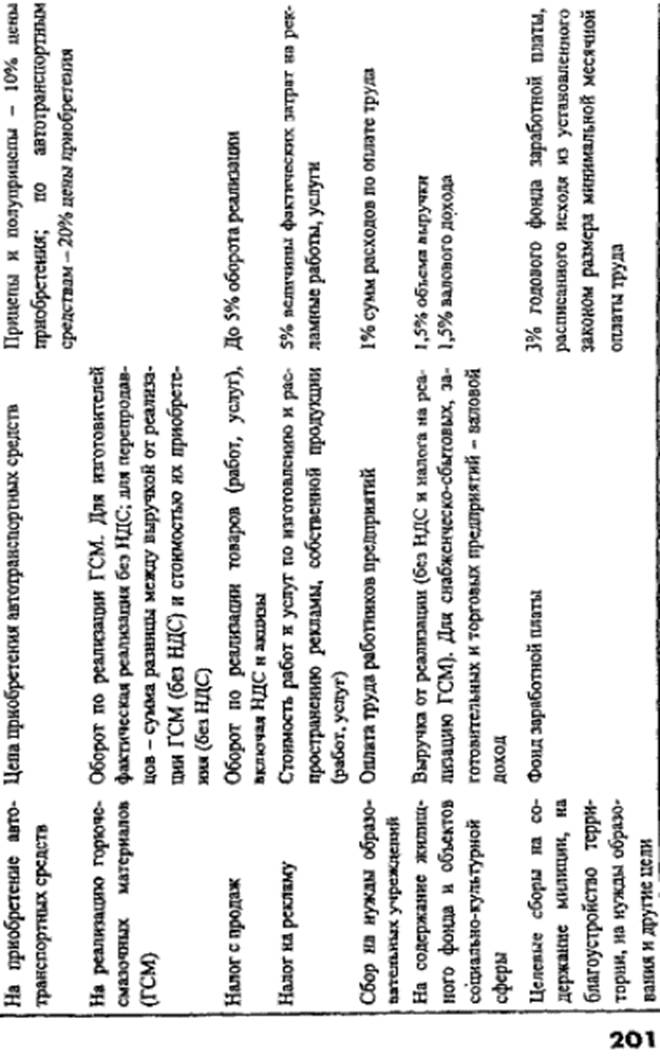

Most small businesses use the usual taxation system, which means they are taxed in the form shown in Table. 6.1.

As you can see from Table. 6.1, there is a large number of taxes and a tax burden.

To the basic features of the current (not simplified) system of taxation of small business can include the following factors:

- High level of tax burden;

- A cumbersome and complex system of accounting and reporting;

- The actual lack of rights of taxpayers before the tax authorities;

- A constant change in tax rates and reporting rules, which makes it practically impossible to forecast financial and economic activities.

Thus, the need for a radical change in the tax policy in the field of small business is obvious.

Control questions

1. What are the principles of building the tax system of the Russian Federation?

2. How are federal taxes distributed among enterprises between budgets of different levels?

3. What elements does each tax contain and in what ways are they levied?

4. What are the main directions for improving the taxation of enterprises?

5. What is meant by tax?

6. Who sets tax rates in the Russian Federation?

7. What functions do the taxes?

8. What is the object of VAT taxation?

9. What is the system of benefits used to calculate VAT?

10. What are excises?

11. What kind of goods are subject to excises and what is the object of taxation?

12. In what terms are excises paid to the budget?

13. Who is the payer of income tax?

14. What is the object of taxation of profits?

15. What are the rates and terms of payment of income tax?

16. What are the benefits for the income tax?

17. What are the benefits of small businesses?

18. Who is the payer of the property tax?

19. What is the object of taxation on property?

20. What enterprises are exempt from property tax payment?

21. List the main taxes paid by small businesses in Russia.

22. Which companies can switch to a simplified taxation system?

23. What is the object and what are the rates of the single tax when the enterprise uses a simplified taxation system?

24. Which document certifies the right of an enterprise to use a simplified taxation system?

25. Who is the payer of sales tax?

26. What is the object of taxation of sales?

Comments

Commenting on, remember that the content and tone of your message can hurt the feelings of real people, show respect and tolerance to your interlocutors even if you do not share their opinion, your behavior in the conditions of freedom of expression and anonymity provided by the Internet, changes Not only virtual, but also the real world. All comments are hidden from the index, spam is controlled.