| home

|

Finance and Statistics - Kovalev AM

7.2 ORGANIZATION WORKING CAPITAL ENTERPRISES

Organization of working capital is fundamental to the whole complex of problems to improve their effectiveness. Organization of working capital includes:

- the composition and structure of current assets;

- establishment of business needs for working capital;

- definition of sources of working capital;

- the disposal and handling of working capital;

- responsibility for the safety and efficient use of working capital.

Under the working capital structure refers to a set of elements that form the current production facilities and handling funds, ie placing them on separate elements.

The structure of the working capital is the ratio of the individual elements of current production facilities and handling of funds, ie, It shows the proportion of each element in the total amount of working capital.

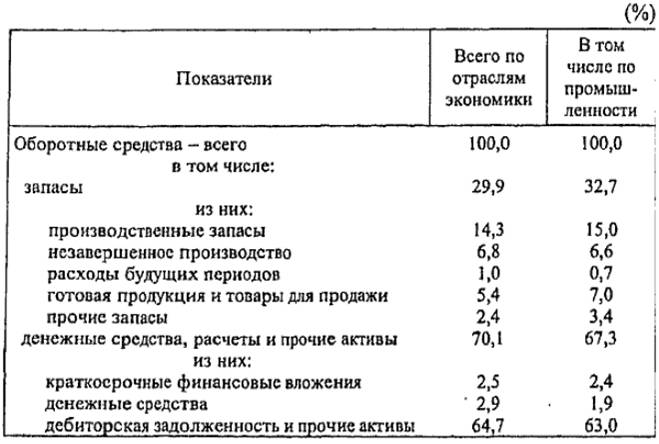

Table. 7.1 shows the structure of working capital of enterprises and organizations established by 1998

Table 7.1

The structure of the working capital of enterprises and organizations

Calculated according to the statistical yearbook of the Russian State Statistics Committee of Russia. - M., 1998. - S. 657.

The prevailing part of the circulating productive assets constitute the objects of labor - raw materials, basic and auxiliary materials, purchased semi-finished products, fuel and fuel containers and packing materials, in addition, to the circulating productive assets are some tools truda- low value items, tools, special tools , replacement vehicles, equipment, spare parts for maintenance, special clothing and shoes. These tools operate at least one year or have a cost limit. Limits cost of funds in circulation change periodically, due to the revaluation of fixed assets carried out and the period of acquisition.

In addition, enterprises these tools often number in the thousands of names that are technically difficult to take into account their wear. Therefore, in practice, they do not belong to the main, and a revolving fund.

These objects and tools form one group of current production assets - Inventories. In addition to them in current operating assets include work in progress and prepaid expenses.

The main purpose of funds advanced in the circulating productive assets, is to ensure continuous and rhythmic production process.

Also circulating productive assets in enterprises formed handling funds. These include: the finished products in the warehouse; goods shipped; cash in hand and enterprises on bank accounts; receivables; funds in other accounts.

The main purpose of treatment is to provide funds resources circulation process.

The composition and structure of working capital are not the same in different sectors and sub-sectors of the economy. They are determined by many factors of production, economic and organizational order. For example, in the engineering industry, where the production cycle is long, high proportion of work in progress. At the enterprises of light and food industry is dominated by raw materials (for example, in the textile industry), at the same time in the food industry (eg, dairy, butter-cheese) are relatively high inventories of auxiliary materials, packaging and finished products.

In enterprises where a large number of used tools, fixtures, appliances, a high proportion of low value items (in mechanical engineering and metal working).

The extractive industries are practically no reserves of raw materials and basic materials for the large proportion of prepaid expenses. In addition, for example, in the oil industry increased proportion of auxiliary materials, spare parts for the repair of fixed assets.

On the value of finished goods, goods shipped, the receivable is influenced by such factors as product sales conditions, forms and status of settlements.

Changing the structure of current assets. It should be noted the continuing trend of repression of the most liquid assets from the working capital due to growth in receivables. At the same time, overdue receivables is about half the total. The main part of the overdue accounts receivable account for the non-state sector of the economy.

Remains high volumes of business debt. At the same time the main share of overdue accounts payable and accounts for the non-state sector of the economy.

It changed the structure of overdue accounts payable. Against the background of mutual non-payments between enterprises increased defaults to off-budget funds.

The main volume of overdue debts to the federal budget, as in previous periods, the company accounted for the industry.

In addition to the separation composition current assets can be classified by the following features.

At the place and role in the process of reproduction distinguish current assets in production and the sphere of circulation.

Consideration of the composition and structure of working capital allows to touch the important problems of the organization of working capital as their rational distribution between the spheres of production and circulation.

Establishing the optimum ratio of working capital in production and circulation is essential to ensure the cash execution of the production program, as well as being a major factor in more efficient use of working capital.

In terms of planning working capital divided into normalized and nonnormable. Domestic practice involves normalization, ie the establishment of the planned reserve norms and standards on the elements of current assets, except for the goods shipped, cash and funds in the calculations. Size not normalized working capital is determined in an expeditious manner.

According to sources of circulating capital are divided into their own, borrowed and borrowed.

In today's economic environment businesses enjoy broad rights available working capital. Current assets at the disposal of companies and not subject to withdrawal. Businesses can sell and transfer them to other companies, organizations, institutions and citizens, to rent, to provide for temporary use (except for those that are not owned or used by enterprises).

An important problem for enterprises is to ensure the safety of the working capital. In the process of financial planning is important to identify the possible presence of a surplus or shortage of working capital at the beginning of the planning period. For this matched the expected amount (actual) presence of own circulating assets of the enterprise at the beginning of the planning period to his total need for working capital. If demand exceeds the planned amount of working capital of the enterprise, there is a lack of working capital. Companies that prevent the formation of a lack of working capital, can make up for it with their own and temporarily borrowed funds.

If the ratio is the opposite, there is a surplus of working capital, which may serve as a source of financing of working capital growth.

Lack of working capital may be due to a number of reasons, depending and not depending on the enterprise. The company can not ensure the safety of existing working capital, ie, lose a certain amount, assuming losses above the plan, the illegal diversion of working capital, for example, to the needs of capital construction, the shortfall in profits.

Economic conditions in which enterprises operate have a significant impact on working capital. Higher prices for purchased goods and materials leads to the formation of the enterprises lack of working capital on a large scale. One of the sources of replenishment is a bank loan, which in the context of inflation is given at high interest rates.

fiscal policy pursued by the state may prevent or promote the normal production and financial activities of companies, including the rational use of working capital. An important role here belongs to the tax policy of the state. Thus, the assignment of a number of taxes to the cost of goods (works, services), particularly the payment of VAT to the budget, advance payments of income tax leads to diversion of working capital of enterprises on non-productive expenditure. This forces companies to borrow at high interest rates, look unplanned sources of funds, to violate financial discipline. The diversion of working capital led to a slowdown of their turnover, reduces the efficiency of the enterprise, its financial condition deteriorates.

Organization of working capital enterprises must include systematic monitoring of their safety and efficiency through the use of audits and inspections on the basis of statistical data, the operational and financial reporting.

Comments

Commenting, keep in mind that the content and the tone of your messages can hurt the feelings of real people, show respect and tolerance to his interlocutors, even if you do not share their opinion, your behavior in terms of freedom of speech and anonymity offered by the Internet, is changing not only virtual, but real world. All comments are hidden from the index, spam control.