| home

|

Finance and Statistics - Ковалева А.М.

7.3 Determination of the need of enterprises for working capital

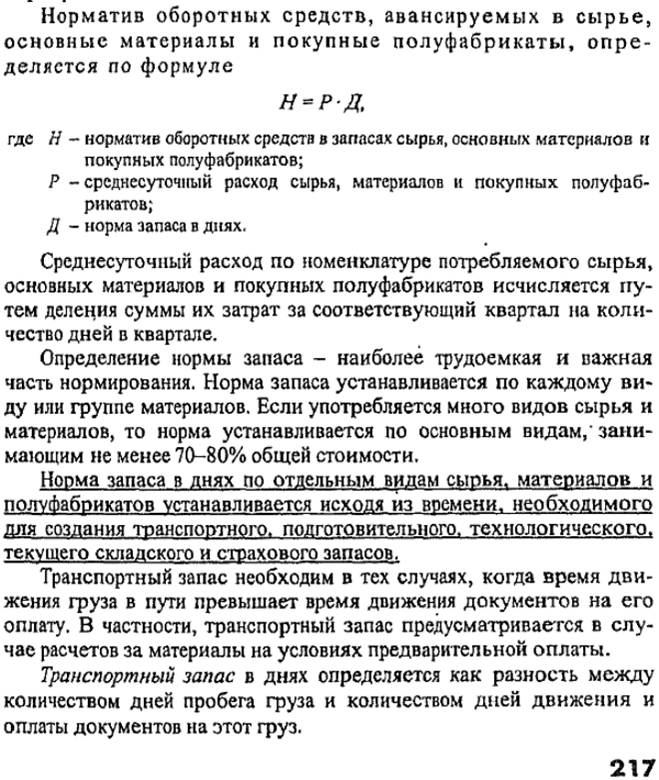

Enterprises that work on the principles of commercial calculation should have a certain property and operational independence in order to conduct business cost-effectively and be responsible for the decisions made. In these conditions, there is a growing need to determine the need for own working capital, which play a major role in the normal functioning of enterprises.

Determination of the enterprise's need for its own circulating assets is carried out in the process of normalization, i.e. Definition of the standard of current assets.

The purpose of rationing is to determine the rational size of working capital, diverted for a certain period in the sphere of production and circulation.

Domestic practice of rationing current assets at industrial enterprises is based on a number of principles.

The need for own working capital for each enterprise is determined in the preparation of the financial plan. Thus, the value of the norm is not a constant. The amount of own circulating assets depends on the volume of production, supply and marketing conditions, the range of products produced, and the forms of payment used.

When calculating the enterprise's need for its own working capital, the following should be taken into account. Own working capital must meet the needs of not only the main production for the implementation of the production program, but also the needs of auxiliary and auxiliary production, housing and communal services and other farms that are not part of the main activity of the enterprise and are not on an independent balance sheet, overhaul carried out by own forces . In practice, the need for own circulating assets for the core business of an enterprise is often taken into account, thereby underestimating this need.

The normalization of working capital is carried out in monetary terms. The basis for determining the need for them is the cost estimate for the production of products (works, services) for the planned period. At the same time, for enterprises with a non-seasonal nature of production, it is expedient to take the data of the fourth quarter as the basis for calculations, in which the volume of production is, as a rule, the largest in the annual program; For enterprises with a seasonal nature of production - the data of the quarter with the lowest volume of production, because the seasonal demand for working capital is provided by short-term loans of the bank.

To determine the standard takes into account the average daily consumption of normalized elements / in monetary terms. According to production stocks, the average daily flow is calculated according to the corresponding item in the cost estimate for production; On incomplete production - based on the cost of gross or marketable products; On finished products - on the basis of the production cost of commodity output.

In the normalization process, private and collective standards are established. The normalization process consists of several successive stages.

First, reserve norms are developed for each element of the standardized working capital. The norm is a relative value corresponding to the stock of each element of circulating assets. As a rule, norms are set in reserve days and mean the duration of the period provided by this type of property. For example, the reserve rate is 24 days. Consequently, the reserves should be exactly as much as will ensure production within 24 days.

The reserve ratio can be set as a percentage, in monetary terms, to a certain base.

Working capital standards are developed at the enterprise by the financial service with the participation of services related to production and supply and marketing activities.

Further, proceeding from the reserve norm and the consumption of this type of inventory, the amount of circulating assets necessary to create standardized reserves for each type of current assets is determined. This determines the private standards.

Finally, the aggregate standard is calculated by adding the individual standards. The norm of circulating assets is a monetary expression of the planned stock of commodity-material assets, minimum necessary for normal economic activity of the enterprise.

Apply the following basic methods for the normalization of working capital: direct account, analytical, coefficient. The method of direct counting is that the amount of advance payment of working capital in each element is first determined, then the total amount of the norm is determined by their summation.

The analytical method is applied in the event that in the planned period there are no significant changes in the conditions of the enterprise in comparison with the previous one. In this case, the calculation of the standard of working capital is made larger, given the ratio between the growth rates of output and the size of the standardized working capital in the previous period.

In the coefficient method, the new standard is determined on the basis of the old by making changes to it taking into account the conditions of production, supply, sale of products (works, services), calculations.

In practice, the most practical application of the direct counting method. The advantage of this method is the reliability, which makes it possible to make the most accurate calculations of private and aggregate standards. Private standards include working capital in production stocks: raw materials, basic and auxiliary materials, purchased semi-finished products, components, fuel, containers, low-value and wearing items, spare parts; In the unfinished production and semi-finished products of own production; In the expenses of future periods; Finished products. The peculiarity of each element determines the specificity of the valuation.

Preparatory stock is provided in connection with the costs of acceptance, unloading and storage of raw materials. It is determined on the basis of established norms or actually spent time.

The technological reserve is taken into account only for those types of raw materials and materials for which, in accordance with the production technology, preliminary preparation of the production (drying, aging of the raw material, heating, sludge and other preparatory operations) is required. Its value is calculated according to established technological standards.

The current stock is designed to ensure the continuity of the production process between the supply of materials, so in the industry it is the main one. The size of the warehouse stock depends on the frequency and uniformity of supplies, as well as the frequency of launching raw materials and materials into production.

The basis for calculating the current stock is the average duration of the interval between two adjacent deliveries of this type of raw materials. The length of the interval between deliveries is determined on the basis of contracts, orders, schedules or based on actual data for the elapsed period. In cases where this type of raw materials and supplies comes from several suppliers, the standard of the current stock is taken in the amount of 50% of the delivery interval. In enterprises where raw materials come from one supplier and the number of material assets used is limited, the standard of stock can be taken as 100% of the delivery interval.

The insurance stock is created as a reserve, guaranteeing an uninterrupted production process in case of violation of the contractual terms of supply of materials (incompleteness of the received lot, violation of the delivery terms, improper quality of the received materials).

The size of the insurance stock is, as a rule, within the limits of up to 50% of the current stock. It can be more if the company is away from suppliers and transport routes, if periodically consumed unique, high-quality materials.

Thus, the total stock norm in days for raw materials, basic materials and purchased semi-finished products as a whole consists of five types of stocks.

The standard of working capital for auxiliary materials is established by two main groups. The first group includes materials consumed regularly and in large quantities. The standard is calculated in the same way as for raw materials and basic materials. The second group includes auxiliary materials used in production rarely and in small quantities. The standard is calculated by the analytical method on the basis of data for previous years.

The general norm of circulating assets for auxiliary materials is the sum of the norms of both groups.

The standard of working capital for fuel is calculated in the same way as for raw materials. The standard for gaseous fuels and electricity is not calculated. When calculating fuel consumption, the need for fuel for production and non-production needs is taken into account. For production needs, the demand is determined on the basis of the production program and the consumption rates per unit of production in the shops; For non-production-based on the volume of work performed.

The norm of working capital by container is determined depending on the method of its procurement and storage. Therefore, the methods of calculating the norms for containers in different industries are not the same,

At enterprises that use the packaging to purchase products, the working capital is determined in the same way as raw materials and materials.

According to the packaging of its own production used for packaging finished products and included in its wholesale price, the stock norm in days is determined by the time of the storage of this container in the warehouse from the moment of its manufacture to the packing of its products. If the cost of tare of own production is not included in the wholesale price of finished goods, but is included in the cost of gross and marketable products, the standard for it is not established, since it is taken into account in the norm for finished products.

By returnable packaging, received from the supplier with raw materials and materials, the working capital ratio depends on the average duration of one turn of the container from the moment of paying the invoice for the container along with the raw material to paying the invoice for the returned packaging by the supplier. The cost of packaging intended for storage of raw materials, materials, parts and semi-finished products in warehouses and workshops is not taken into account when determining the standard of working capital by packaging, as it is part of fixed assets or low-value and wear items.

The norm of circulating assets for spare parts is established for each type of spare parts separately, based on the terms of their delivery and the time of use for repair. The standard can be calculated on the basis of standard norms per unit of book value of fixed assets, by an analytical method based on the data of previous years.

The standard for low-value and wear items is calculated separately for tools and devices, low-value inventory, special clothing and footwear, a special tool and attachments.

According to the first group, the standard is determined by the direct account method based on the relying set of low-value and fast-wearing tools and its cost. The second group sets the standard separately for office, household and production inventory. The standard for office and household inventory is determined based on the number of seats and the cost of inventory for one place; On production inventory - based on the need for a set of this inventory and its value.

The standard of working capital for overalls and footwear is determined on the basis of the number of employees they rely on and the cost of one set. The standard for this group of working capital in the warehouse is determined by multiplying the one-day expense by the stock norm in days, including transportation, current and insurance stocks.

By special inventory and adaptations, the standard is determined on the basis of their relying set, cost and service life.

At enterprises that have a small share of low-value and short-wearing items in the structure of working capital, the standard is calculated on the basis of the ratio of the average actual reserves to the amount of production costs.

The standard of working capital in the work in process is to provide a rhythmic production process and a uniform supply of finished products to the warehouse. The standard expresses the cost of products that have been started, but not finished, at different stages of the production process. As a result of the normalization, the value of the minimum reserve sufficient for the normal operation of the production should be calculated.

The amount of working capital advanced to the work in progress is not the same for enterprises and industries. The main reasons for the differences are the characteristics of the organization, the volume of production, the structure of the products.

The normalization of working capital in the work in process is carried out by groups or types of products for each unit separately. If the assortment of products is diverse, then the standard is calculated on the basis of the main product, which is 70-80% of its total mass.

The standard of working capital in the work in process is determined by the formula

H = P-T-K,

Where Р - one-day costs for production;

T - duration of the production cycle in days;

K - coefficient of increase in costs.

One-day costs are determined by dividing the cost of output of the gross (commodity) output of the corresponding quarter by 90.

The product of the duration of the production cycle by the coefficient of increase in costs is the stock norm in days under the item "Work in progress".

The duration of the production cycle reflects the time of the product's stay in the work in process from the first technological operation to the complete manufacturing of the product and its transfer to the warehouse.

The technological cycle includes the technological stock (the time of processing the product), the transport stock (the time of transfer of the product from one workstation to another and the warehouse), the turnover stock (the time of the products stay between processing operations) and the insurance stock (in case of delay of any operation ). When calculating the standard, the production cycle is determined for each type of product in calendar days, taking into account the number of shifts in the work of the enterprise per day. At enterprises that produce a wide range of products, the duration of the production cycle is defined as the weighted average.

The coefficient of increase in costs reflects the nature of the increase in costs in the work in progress by the days of the production cycle.

All costs in the production process are divided into one-off and incremental. The one-time costs include the costs incurred at the beginning of the production cycle (costs of raw materials, basic materials and purchased semi-finished products). The remaining costs are considered to be increasing (depreciation of fixed assets, energy costs, labor costs, etc.).

Finished products manufactured at the enterprise characterize the transfer of working capital from the sphere of production to the sphere of circulation. This is the only normalized element of circulation funds.

The norm of circulating assets for finished products is determined by the formula

H = PxD,

Where

Р - one-day output of commodity production at the production cost;

D is the stock norm in days.

The norm of circulating assets for finished products is determined separately for finished goods in the warehouse and for goods shipped, for which settlement documents are in registration.

The norm for finished products in the warehouse is determined by the time of acquisition and accumulation of products to the required sizes, storage of products in the warehouse before shipment, packaging and labeling of products, delivering it to the dispatch and shipment station.

The norm for goods shipped for which documents are not submitted to the bank is determined by the established terms for issuing invoices and payment documents, submitting documents to the bank, the time of transfer of amounts to the accounts of the enterprise.

Thus, private standards are established for each element of the standardized working capital. Then the cumulative norm of circulating assets is determined, reflecting the general need of the enterprise for its own circulating assets in the planned period, by adding individual norms.

Further it is necessary to compare the received cumulative normative with the cumulative norm of the past period in order to determine how the enterprise's need for its own circulating assets changes in the planning period.

The difference between the norms is the amount of growth or decrease in the standard of working capital, which is reflected in the financial plan of the enterprise.

Comments

When commenting on, remember that the content and tone of your message can hurt the feelings of real people, show respect and tolerance to your interlocutors even if you do not share their opinion, your behavior in the conditions of freedom of expression and anonymity provided by the Internet, changes Not only virtual, but also the real world. All comments are hidden from the index, spam is controlled.