| home

|

Finance and Statistics - Kovalev AM

9.2 FINANCIAL ASPECTS OF THE DEVELOPMENT OF ENTERPRISE BUSINESS PLAN

Analyzing the domestic experience on the business plan, it can be concluded that all of its sections the least developed is rightly considered a financial plan. In this regard, we emphasize how great the role of methodical support is the financial part of the business plan. Because this chapter deals only with the financial aspect of its preparation, ostanovimsya- on presentation of this problem.

the financial section of the business plan includes the development of the following standard documents:

to forecast financial results.

© The need for additional investment and the formation of sources of funding.

® discounted cash flow model.

in the break-even point (break even point).

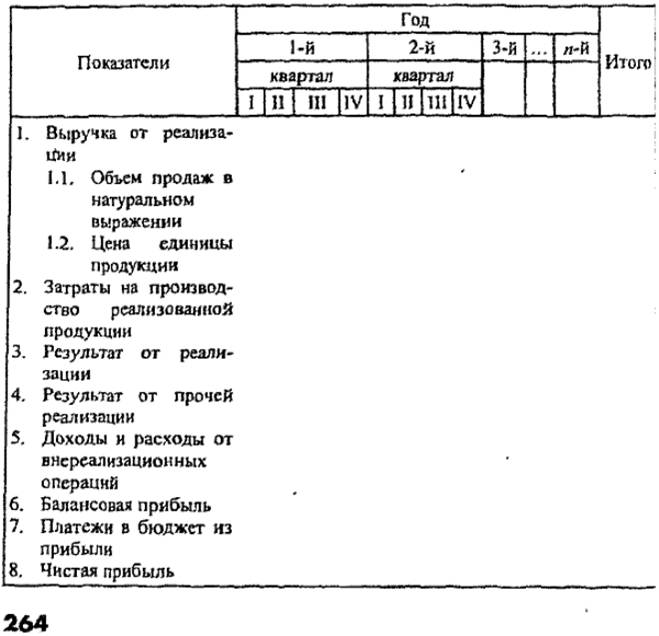

Forecast financial results are invited to establish in the following form (tab. 9.1). Read more about the directions of the financial recovery of enterprises cm. In Sec. 10.

Table 9.1 Forecast of Financial Results

It is proposed to develop the financial section of the business plan proceed from the fact that the definition of the funds needed to finance the company's development, involves the assessment of the plan as an investment project. This means that provided the business plan of the enterprise costs must be justified by their economic efficiency.

Forecast financial results will only be valid when reliable information on the growth prospects of key performance indicators, the dynamics of which has been proved in other sections of the business plan. Revenue from product sales is determined based on the forecast sales volumes for the planned year i'prognoznyh prices. Naturally, because of the large range of products proceeds from the sale may be given only in total, not in relation to the same type of product.

sales forecasting, production costs of goods sold, the results from other sales, income and expenses from non-sales operations, as well as payments to the budget from the profits of the enterprise should take into account the possibility of seeking additional reserves of growth of production and sales. Such additional features may appear in the company at the stage of implementation of the program of work to develop and implement a business plan, which as an example is made taking into account the industry characteristics of the fuel and energy complex. It is given in Appendix 1.

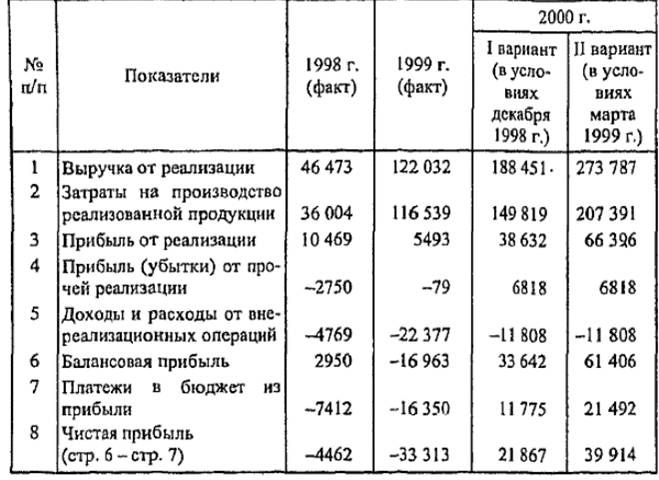

For a realistic assessment of additional financial opportunities identified in the analysis of financial and economic activity of the society, it is useful to make this assessment in several different ways. Table. 9.2 presents forecast of financial results for the Open Joint Stock Company "Saratovneftegas" for 2000 in two variantah1. The first option gives you a forecast based on actual economic conditions (especially the price of oil and gas), in which the society was in December 1998. The second version takes into account the actual conditions in March 1999 It is tougher as sharply increased payments in the budget, the cost of production of sales at constant results from other sales and non-sales operations. Net income grows more slowly.

'These conditional.

Table 9.2

Forecast financial results of JSC "Saratovneftegas" for 2000

(thousand Roubles.)

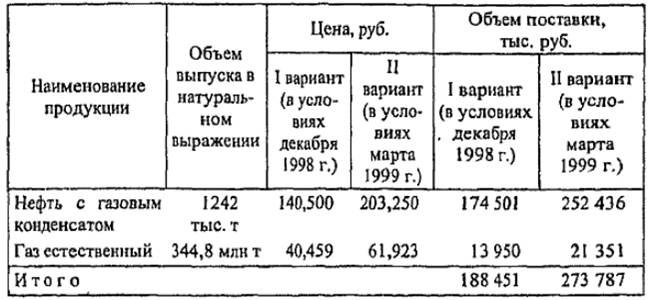

The greatest influence on the accuracy of the forecast financial results have planned the delivery of basic production and the cost of its production. So it makes sense the dynamics of production also count in comparable cases. Table. 9.3 is planned volume of supply of products by JSC "Saratovneftegas" for 2000 Terms of payment chosen comparable in December 1998 and March 1999 Proportions increased supply of products (oil, gas) approximately correspond to the dynamics of the projected financial performance that It indicates the validity of the forecast,

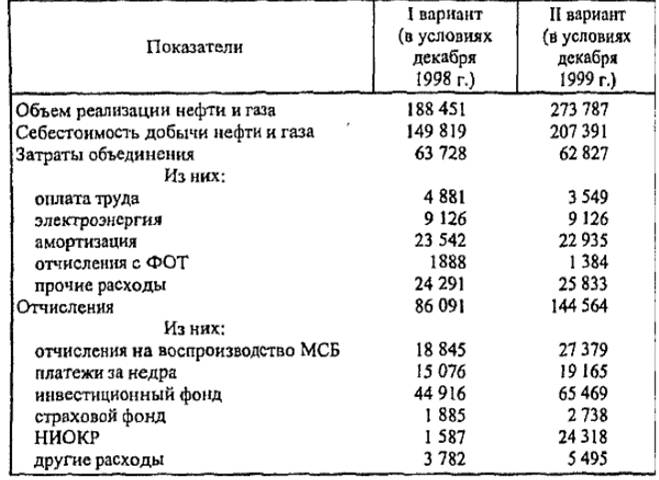

Similarly, the two options are considered costs of main production at JSC "Saratovneftegas". Estimated cost of oil production and gas is given in Table. 9.4. The increase in the cost of oil and gas production, labor costs and planned contributions to the largely confirm the reality of income growth association except research and development activities. the latest costs increased from 1587 thousand. rub. I option on up to 24 318 thousand. rub. for embodiment II, i.e. more than 15 times. At the same time, II version of the calculation for the entire amount of deductions made their growth is only 1.7 times, and cost growth are respectively 1.4 times. Investments in R & D can be critical to the further development of production and improve its financial results.

Table 9.3

The planned volume of supply of products by JSC "Saratovneftegas" for 2000

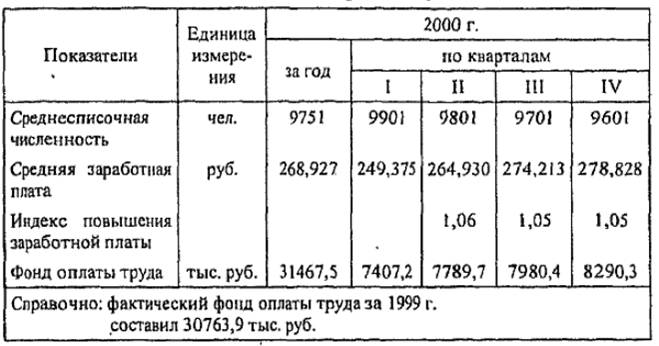

The most hard to predict the directions in the development of a business plan, in particular in the calculation of projected financial results include the determination of the required payroll. Insufficient social security community workers does not allow the board of directors of enterprises pursue a policy of strict wage freeze. Delays in the payment of wages in the crisis have become a frequent occurrence. The loss of workers at the same time due to inflation are big enough. At the same time increase wages only if increased profitability.

Table. "Saratovneftegas" 9.5 is the estimated wage fund for 2000 to the public limited company. Compared to 1999, the wage fund increased slightly according to the scheduled data, ie, with 30,763.9 thousand. rub. to 31,467.5 thousand. rub. Recall that the revenue from the sale of products is planned for the II variant is based on 24%.

Table 9.4

Estimated cost of oil production and gas joint-stock company "Saratovneftegas" for 2000

(thousand Roubles.)

Discounted cash flow model is based on the forecast of the results of financial and economic activity. The total financial result is calculated as the sum of the discounted (ie, reduced income, increasing for a definite period according to the formula of compound interest) cash flows for each year of implementation of the financial recovery plan, and current discounted residual value beyond the planning period.

Emphasis on a discounted cash flow model and turn it into a business plan is determined by the fact that many of the costs displayed in the forecast of financial results are not reflected in the order of payment. For example, the materials can be paid for long before these costs will fall in the forecast profit and loss. Separate payments are made quarterly or annually. Therefore, the data for those months in which they are produced may be significantly larger than the other.

Therefore, we can conclude that the profit does not always mean an excess of money in the current account and on hand and cash surplus does not mean that the company makes a profit. In the context of the insolvency of enterprises it can be a very serious problem, since even an excess cash is not yet profitable work. In the presence of large overdue payables enterprise may have significant financial difficulties.

Table 9.5

Estimated salary fund for 2000 for JSC "Saratovneftegas"

The main task of the forecast by compiling a cash flow model is to check the synchronicity of the income and expenditure of funds, check the future liquidity of the company.

In addition to these documents in a business plan and a graphical analytically determined the break-even point (break even point). To determine this point, regardless of the method used must first divide the projected costs of permanent (conditionally constant), do not depend on changes in the volume of production, and variable (semi-variable, the value of which changes with the growth or reduction of the volume of production). profitability threshold is defined as revenue from sales, in which the company no longer has

sponding their effective functioning - should be primarily attributed to the absence of a strategy of enterprises, as well as special methods and techniques of financial management. The development of enterprise development of business plans in such uncertain conditions, often not justified.

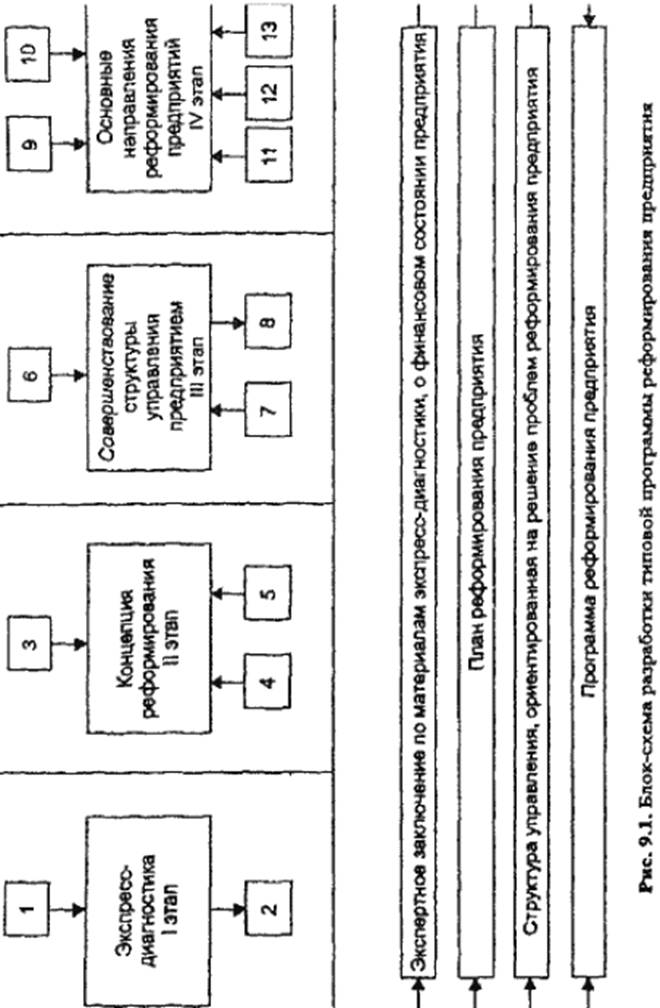

Fig. 9.1 is a block diagram of a typical development of the enterprise reform program. It consists of four main stages of work, and 13 within them separate types of work.

I stage. Express diagnostics.

1. Setting a computer program for rapid

diagnosis of the enterprise.

2. Training of the personnel regularly use

a computer program for the rapid diagnosis of balance sheet data.

Stage II. The concept of reforming.

3. The mission of the company.

4. The main objectives and tasks.

5. Management by Objectives.

Stage III. Improving the management of the enterprise structure.

6. Analysis of the current management structure.

7. Changes to the current management structure in

accordance with the objectives of the enterprise reform.

8. Clarification of the provisions of the departments and services of the enterprise and

job descriptions of its employees.

Stage IV. The main directions of the reform of enterprises.

9. Guidelines for the development of supply and marketing policy of the enterprise.

10. Guidelines on the development of the price policy of the enterprise.

11. Guidelines on the development of financial recovery plan.

12. Guidelines on the development of the investment policy of the enterprise.

13. Guidelines for the management of the personnel.

In line with the objective block diagram a typical design of the enterprise reform program are executed sequentially each step included in the list of this stage of work performed. In this business plan actually becomes final planning document implementation of typical enterprise reform program.

Fig. 9.1. Block diagram of a typical development of the enterprise reform program

Comments

Commenting, keep in mind that the content and the tone of your messages can hurt the feelings of real people, show respect and tolerance to his interlocutors, even if you do not share their opinion, your behavior in terms of freedom of speech and anonymity offered by the Internet, is changing not only virtual, but real world. All comments are hidden from the index, spam control.