| home

|

Finance and Statistics - Ковалева А.М.

12.2 CAPITAL, PROFIT AND FUNDS OF JOINT-STOCK COMPANY

With the establishment of the JSC, its charter capital is created, reflecting the minimum amount of the company's property that guarantees the interests of its creditors. The authorized capital of an AO consists of a certain number of shares, the number of which is stipulated in the charter. In accordance with the law on joint-stock companies and the Civil Code of the Russian Federation, the nominal value of shares acquired by shareholders is included in the charter capital of the JSC. In this case, all common shares have the same nominal value. Along with ordinary shares, AO has the right to place preferred shares. However, their nominal value should not exceed 25% of the charter capital of the company.

Shares issued by the company, but not paid for by shareholders, can not constitute authorized capital.

The authorized capital is not identified with the value of the property transferred by the founders of the company (buildings, structures, equipment, securities, money, property rights to use land, water, natural resources, intellectual property, etc.), which may be more or less than the authorized capital ,

The minimum amount of the authorized capital is determined by the law on joint-stock companies. For societies of open type, it is not less than a thousand times the amount, and for closed societies - not less than a hundred times the minimum monthly wage established by law on the date of state registration of the JSC.

The value of the authorized capital at the establishment of the joint-stock company should be fully distributed among the founders. At the time of establishing AO, shares for open subscription are not allowed, i.e. Public sale. All shares must be fully distributed among the founders.

Payment of shares and other securities. Shares that are an integral part of the share capital are paid as follows. At least half of the shares are payable by the time the AO is registered. The second half must be paid within a year of the registration of the company. Additionally issued shares must be paid not later than one year from the moment of their acquisition.

According to the decision of the founders and management bodies of the joint-stock company, the form of payment for shares and other securities of the company can be effected by money, securities, property and other rights that have a monetary value.

When paying for additional shares issued in cash, the share of this payment should not be less than 25% of their nominal value. When paying for shares and other securities by non-monetary means, payment is made in full amount of their value. The property contributed to the payment of shares for the creation of joint-stock companies is assessed on the basis of an agreement between the founders, and subsequently when paying for the additional issue of shares and other securities - on the basis of a decision of the board of directors.

If the nominal value of shares and other securities purchased from non-monetary funds exceeds 200 times the minimum monthly wage, the property is valued by an independent auditor. To stimulate timely and full payment of the authorized capital, the share does not give the right to vote until it is fully paid. The exception is shares paid by the founders of the company when it is created.

With partial payment of shares in the specified time, the shares are placed at the disposal of the JSC. When shares are paid after the expiration of a certain period, the received money or property is not returned by the company. Moreover, in the charter of joint-stock companies it may be envisaged to collect penalties, fines and penalties from non-payers.

Unpaid and received at the disposal of the company shares are subject to sale in a period not later than one year, otherwise by decision of the general meeting of shareholders they must be repaid with a corresponding reduction of the authorized capital.

The authorized capital should not exceed the value of net assets.

Net assets of the joint-stock company are estimated in accordance with the legislation on the basis of accounting data. To determine the value of net assets from the total assets of the joint-stock company, its liabilities are excluded, except for liabilities on shares.

The state of joint-stock companies depends on the ratio of net assets and authorized capital. If, after the second and subsequent financial years, it is revealed that the amount of the company's net assets is less than its authorized capital, the company is obliged to declare a corresponding decrease in its authorized capital.

If the value of net assets is less than the minimum authorized capital, established by the law on joint-stock companies, the company is subject to liquidation.

Change in the authorized capital of the joint-stock company. The initial amount of the authorized capital is determined by the founder when creating the joint-stock company. In the process of functioning of the company, the authorized capital may vary. Due to the growth of profits or additional contributions of founders, it can increase and, conversely, with a reduction in profits and other factors, it may decline. In any case, the change in the share capital in one direction or another can be made only on the basis of a resolution of the general meeting by a majority of votes. However, this decision comes into force only after registration authorities are notified of this.

The increase of the authorized capital can be made only after the full payment of the initial authorized capital.

The authorized capital of the joint-stock company is increased by issuing new shares or increasing their nominal value.

The increase of the authorized capital of the company is possible after full payment of the initial authorized capital.

The additional issue of shares can be carried out only after the approval by the general meeting of the results of the previous issue, the introduction of changes in the authorized capital due to the actual sale of previously issued shares and the repayment of unrealized shares. With an additional issue of shares, the shareholders owning the voting shares have the pre-emptive right to acquire them. The number of issued additional shares should not exceed the number of such shares provided for in the charter of the company.

The charter capital of the JSC can be increased not only by additional issue of shares, but also by changing the nominal value of shares. In this case, all categories and series of shares issued by AO, as well as liabilities on options and convertible bonds issued before the decision to increase the authorized capital, are changed in equal proportion.

The increase in the authorized capital may occur as a result of the exchange of convertible bonds for shares, the return of shares held by subsidiaries, the return of a portion of shares and? Reserve fund.

The increase in the authorized capital is also made as a result of revaluation of fixed assets through additional issue of shares or by increasing the nominal value of the issued shares.

Decrease in the authorized capital of the joint-stock company is carried out by reducing the nominal value of shares or redemption of shares to reduce their total number. The possibility of reducing the authorized capital by acquiring and redeeming a portion of shares must be provided for in the company's charter. However, the authorized capital can not be reduced to a size lower than the statutory minimum authorized capital. Only shares that are on the balance sheet of AO can be redeemed, including shares acquired for this purpose from shareholders.

A decrease in the authorized capital of an JSC can be made not only through the repurchase of its own shares, but also the exclusion of shareholders and the return of their contributions, by reducing the amount of subscription to the actually paid-up value of shares. The authorized capital is also reduced when shares are transferred to subsidiaries, as well as when part of shares are transferred to the reserve fund.

A decrease in the authorized capital of an AO can be made only after the notification of all creditors of the company. Written notification of creditors is made within a period not later than 30 days from the date of the decision of the general meeting. Lenders have the right to demand early termination or performance of obligations, as well as compensation for losses from a decrease in the authorized capital.

Profit of the joint-stock company. Profit AO is formed in the same way as at enterprises of other forms of ownership, in the form of the difference between the proceeds from the sale of products (works, services), minus the corresponding taxes, and the costs of production of these products (works, services).

If costs exceed the amount of revenue, the company has losses. The procedure for using profits not subject to distribution among shareholders is determined by the company's charter. After the payment of the profit tax and other mandatory payments, there remains a net profit coming to the full disposal of the JSC.

Distribution of net profit and indicators of the financial condition of the joint-stock company. The Board of Directors decides on the distribution of net profit. A part of this profit may be directed to the production and social development of employees of the joint-stock company in the form of cash rewards or shares of the company, The share of profit for payment of interest on bonds is determined. Deductions are made to the reserve and special funds. The possible emissions are calculated in accordance with a certain percentage

Volume, provided by the charter. The remaining net profit is used to pay dividends to shareholders.

The Board of Directors, taking into account the financial condition of the company, the competitiveness of its products and prospects for development, decides on the specific ratio of the size of the net profit distributed in these areas. It is not excluded that in certain periods the profit will not be directed to the payment of dividends to shareholders, but in a larger amount will go to the production and social development of the work collective or other purposes.

The company's shares on its balance sheet are not taken into account when dividing profits between shareholders.

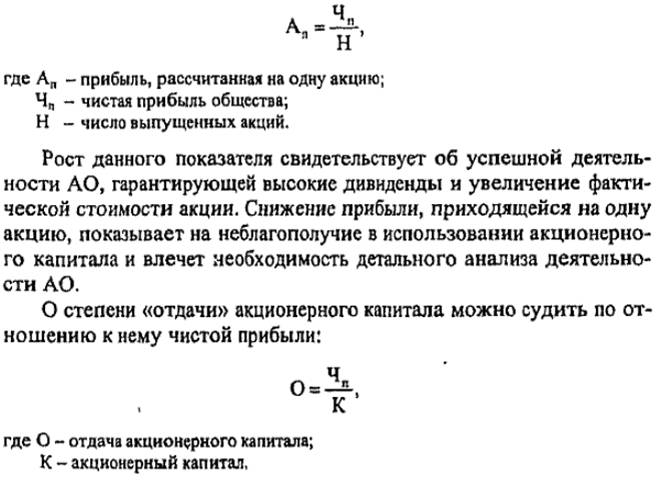

One of the indicators characterizing the financial condition of the JSC, which determines the process of profit distribution, is the share of profit calculated for one share.

The size of the net profit attributable to one share makes it possible to really assess the efficiency of the JSC's activity, its financial position. Such an indicator is calculated by the formula

The indicator of return of the share capital characterizes intensity of its use and, hence, growth or reduction of the profit received from this capital.

Reserve and other funds of the joint-stock company. In the process of distributing the net profit of the joint-stock company, a reserve fund is created, the value of which should not be less than 15% of the authorized capital. The procedure for the formation and use of the reserve fund is determined by the charter of the JSC. Specific amounts of annual deductions from profits to the reserve fund are provided for in the charter, but not less than 5% of the net profit of the company.

Formation and replenishment of the reserve fund occurs through annual deductions up to the achievement by this fund of the amount provided for by the charter of the company. The reserve fund is intended to cover unforeseen commercial losses of joint-stock companies. Due to this fund, bonds are redeemed and shares are redeemed in the absence of other funds. The use of the reserve fund for other purposes is prohibited.

At the expense of net profit, a special fund for the corporatization of company employees can be established. However, this should be provided by the charter of the JSC. The funds of this fund are intended solely for the repurchase of shares of the company sold by shareholders and their further placement among their employees.

The possibility of creating the corporatization funds is stipulated in the law on joint-stock companies based on the experience of the formation of such funds from open joint-stock companies formed as a result of the privatization of state and municipal enterprises.

Comments

Commenting on, remember that the content and tone of your message can hurt the feelings of real people, show respect and tolerance to your interlocutors even if you do not share their opinion, your behavior in the conditions of freedom of expression and anonymity provided by the Internet, changes Not only virtual, but also the real world. All comments are hidden from the index, spam is controlled.