| home

|

Insurance and Investment Management - Fedorenko V.G.

11.4. MANAGEMENT OF PORTFOLIO OF FINANCIAL INVESTMENTS

At підприємницькій діяльності ризик по'язується з фінансовими втратами, щ о стають неминучими в разі реалізації пвних ризиків.

Усі вид ризиків, влаві тим чиіншим цінним паперам, - відсотковий, крединий, діловий, інфляційний, дострокового погашення, ліквідності, - in the form of a jagged rizik of a technical tool, a way to get rid of yogo dohіdnіstyu. Rizik polyagaє in that, scho ochikuvannya vlasnika schodo rіvnya dohіdnostі tsіnnih papperіv mozhut not sravditišis і yakus ogonu budin v budetcheno. At the time of the examination of the points of the dohd, and the subordinate rizik is rooted, the invisibility of the schodo can be otrimannya zhogo income, tobto yak riven mіnivisti (varіabelnosti) income. Otzhe, dohіdnist portfolio, yaku priodivayatsya yogo vlasnik, є vipadkova value, and that yogo kilkisna otsinka can not be unambiguous. Do tsilomu vimiryugannya riziku fіnansovyh іnvestitsіy є bagatoaspektnoyu problem yak z poglyadu techniques analizu, so iz z posetsі efektivnogo upravlennya інвестиційним портфелом.

On the practical level, for the sake of the world, the rizikomu vikorystvuyut riznomannіtі pokazniki, yakі, in the main, are represented by statistical values, such as dispersion, standard vidhilennya, koefіtsіnti korelyacії i kovarіatіїї. The characteristics of a particular papermon are shown, in the past, in the form of an actual dentistry of yoga, actual docility can be observed in all cases. The magnitude of the risk should be based on the baseline analysis of the real data about the prehistory of the papernis after the transitional period for the statistical methods. Briefly, the main statistical indicators of rizikovesti are characterized.

Naichastishe at protsessi analizu riziku tsinnogo paperu vikoristovyot koefitsynt in (beta). For naremogo tsinnogo papper in rozrachovuyot yak vidnoshennya kovarіаcії dohіdnostі papperu ta rinku v tsilomu do dispersії дохідності ринку:

De in - the beta of the paperns; Cov (P, R) - covariation of the price of a paperman of the R-mark R; R is the dispersion of the zinc.

Kovarniatsya zmіnnih R і R calculates for the formula:

De R, I - the middle of the range.

Коефіцієнт кореляції (рРЯ) показує щільність залежності між двома in rows динаміки і розраховується за формулою

De Or_ ak - standard vіdhilennya дохідності відповідно цінного паперу та ринку.

Standard vidhilennya show, naskilki broad є riziv Mizh znachennami specific sposterezhennya ta serednіm znachennyam number, і enumerate for the formula

De Rí, - meaning to the income of a regular paperman in, -my sporestrazhenny; P is the middle of the series; N - kilkіst sposstrezhen.

Standardnoe vidhilennya dohіdnostі rinku obkchylyuetsya analogіchno. The square of the standard vidhilenya nazivayutsya dispersion.

Yak bachimo, for rozraunku koefіtsіnta in neobhіdno mati danі about dinamiku rinkovoi dohіdnostі tsinnogo paperu. Yak rule, such a showman vvazhayut fondovy iindeks, yak korostusteyatsya naybіlshoyu populyarnіstyu on a particular market. On the international markets, the Standard & Poor's, the impetus for the basics of the dinamics of the financial markets, the S & P 500 index, on the markets of Japan - the Nikkey index. The information about the docility of investment in the capital is on the basis of the results of an analysis Співвідношення дохідності та ризику, в результаті якого визначається, чи бытня очікувана дохідність цінного паперу для компенсації по'язаного з ним ризику. Ale is more interested in investor than in one, but with a small number of private papermen, who in the form of a portfolio. Vlastistosty portfolio vidriznyayutsya vid power vzrymih tsinnyh paperiv, zokrema schodo viznachennya rivnya risiku.

Theory of the effective portfolio of financial investments, yaku vpershe rasprobiv G. Markovits in the 50th rock of the last table, zhdomom sutesto vskonaliili R. Traynor, J. Lintner, U. Sharp that інші. Розглянемо основні її положення.

Дохідність portfolio є aditive value і дорівнює сумі доходів, що їх генерують окремі цінні папери. Середня rate дохідності портфеля (dp) визначається як середньозважена The size дохідності фінансових інструментів, що въть до його складу:

De ji - the availability of the i-th species of the paperns (i = 1, ..., n); Ї? І - the osnag tsinnyh papperіv і-th mind in the portfolio; П - кількість видів цінних паперів у портфеліі.

At the time of the crisis, the portfolio risk is not obovyazyovo vimiryuyutsya srednnozvazhenoyu amount of sukupnost rizikіv okremih portfolioovye, oskilki rіznі vіnch tsіnnih paperyv in a rіznym reaguyut zmіynu konjunkturi rinku. Standard vіdhilennya дохідності цінних паперів у багаох випадках mozhet vzasemno zakupashiysya, the result of chоgo стає зниження загального ризику портфеля за збереження його дохідності. Отже, ризик портфеля значною мірою залежатиме від кількості видів цінних паперів, yakі formyut portfolio, that's the way, наскільки і в якому підмку змінюється їх дохідність за зміни коньюнктури ринку.

In the process of analyzing the portfolio, a viokremluvati of two warehouses was put in place: a systematic and unsystematic risk.

Systematic risk - part of the fatal systemic risk, to be located in the economy of the economy in the future and in the macroeconomy, such as the taxation of investments, the obligations of the citizens, the payment of taxes, the balance of payments, and that it is in the presence of all the subordinates of the state Process. Systematic risik nazivayut nondiversifikovaniem, aboninkin, yokogo yokogo can not change the diversification (included before the portfolio of the plies for the characteristics of the paperns). Otzhe, divver-sifikovy portfolio to characterize the systematically risky, a kind of vimiryuyut for dopomogo koefіtsіnta beta (c).

An unsystematic risk has been attributed to the lack of identity of the specific capacity of the census paperns. Інвестор має змогу уникнути цього ризику, извіввіть єффінний portfolio, тобто such набір цінних паперів, який уможімлює взаємне коменсування коливання дохідності різних інструментів, if there is a shortage of additional information for a one-year-old papper, you can compensate for a pre-existing loss of life. To reduce the risk of unsystematic risk and dystopia, the method of diversification. Rizik nediversifikovogo portfolio vimiryuetsya standard vidhilennnyam.

The beta for the portfolio in the middle (RR) is rooted in the middle of the value of the beta values (vі) quietly visible in the paperns, but enter the yogo store, and destroy the pythonage vagas in the portfolio structures. Slid nagoloshiti on that, scho kozhen a kind tsinnyh paperyv moe vlasniy koefitsynіt vі, yakі є індексом дохідності цього ціоного паперу що середьої дохідності on the stock market. Otzhe, yakshto to the portfolio of the portfolio of pidpriemstva included rіznі vіnych tsіnnih papperіv, then the beta is to be voznachaetsya okremo for kozhny z them (11.15), після чого рр обчислюють за формулою

De Rr - a factor of beta і-th species of pinnipeds, but enter the portfolio warehouse; Уі, Рі - the pythoma of the vaga- і-th type цінних паперів у портфеліі; Р - кількість видів цінних паперів у портфелі підприємства.

Коефіцієнт Рр показує, наскільки зміниться дохідність portfolio for зміни очікуваної дохідності ринкового портфеля на 1%. To take a rink portfolio for the Odinitsa Rp. For a portfolio of PP <1 zmіni konjunkturi, the market is less likely to become familiar with the yogo prejudice, natomist the income of the portfolio> 1, to increase in size, nizh dohіdnіst усього ринку. Primir, yakshcheo Рр = 1,3, then for the growth of the preindustrial market by 2%, the portfolios of the portfolio grew by 2.6%. For znizhennia дохідності ринкового портфеля на 2%, the portfolios of the pre-stock of such a portfolio are to be replaced by 2.6%, so that the promising rivin is reduced to the risk of a portfolio of medium-sized risks. For znachennyam beta portfolio subscribe to the aggressive (vp> 1) that zahisni (vp <1). Якщо вр = 1, then the risk of the portfolio is reduced to the system level. Znachennya beta mozhe bouti not tilki dodatnim, and th vіd'ємним. Tse means, ucho dokhidnist rinku і portfolio tsinnyh papernіv, sformovanogo by the investor, zminuyutsya at protnyzhnih strains.

In the process of managing a portfolio before an investor, post-installment of a loan is made in order to reduce the risk of the portfolio. Нині найуживанішою є the technique of analysis of the basin in the basics of the model of the capitalist active activities (CAPM). Відповідно до основних положень моделі САРМ дохідність портінних паперів (др) розглядається yк functція трьох змінних: systematic portfolio risk (ВР), ochikuvanoї дохідності портфеля (іт) та rate of income for bezryzikovymi цінними паперми (й0). Залежність між очікуваною дохідністю та ризиком виражається формулою

For the economical zmistom perevischennya dohіdnosti portfolio over the risk-free rate є premiєyu, scho її otrimuє yogo vlasnik for risik, yaky vyn sez on himself, pridbavi pevnі tsinnyi paperi at the process of formulating the portfolio.

On the basis of the model, the analysis of the efficiency of the management of portfolios. Коефіцієнт ефективності розраховується як відношення різниці між дохідністю портфеля (реальною або очікуванію) та безризиковою with the rate to the forexample, а я відбражає ризик портфеля. In the case of management, the kul'ka koefіtsієntіv efektivnosti, yakі mozhut bouti vikoristani u protsessi analizu ta priinyattya upravlinskih rіshen. In order to regulate the efficiency of managing the portfolios of private paperns, one should be able to wipe out the same structure, allege through the ways of making money in a portfolio.

In the process of analyzing the effectiveness of a diversified portfolio, often the curriculum of a trainer (kT):

De - the availability of the portfolio of the investor for the period, and the analysis.

Co-ordination Sharpa dotsilno zastosovuvati for analizu nediver-sifikovanogo portfolio tsinnih paperyv (k5):

Де ср - стандарне відхилення дохідності of portfolio of the investor.

Methodology vyznachennya koefіtsієntіv efektivnosti upravlennya portfolios tsinnyh paperіv ta їх порівняльний аналіз про demonstструємо butt.

Application 8

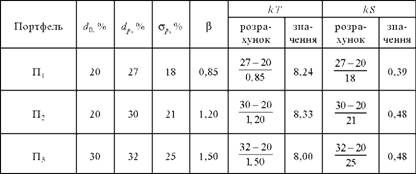

Pідприємство має three varіанти of the form of the portfolio of financial investments (П1, П2, П3), the main characteristics of which are indicated in the table 11.5. Necessarily proanalizuvati portfolio with a glance spivvodnoshennia "дохідність - ризик" та вибрати оптимальний. Analiz efektivnosti portfolios conducted for the sake of the curriculum of Trainor and Sharp.

Yaksho before the pidpriemstvom postaet zavdannya viboru optimal

Of the portfolio of positivities with the "prehistory - rizik", and the portfolio

Table 11.5

Analiz koefіtsієntіv efektivnosti upravlennya portfolios tsіnnih papperiv

Proanalizovano for koefitsyntom Traynor, then perevagu slid viddati another portfolio. Якщо ж аналіз здійснено за кефіцієнтом Шарп, then on the subject of the effectiveness of the management of the other and third portfolio, they were vividly imagined, and on the odnitsynu risiku pidpriemstvo matima 0.48 oditnits vinogradov. Zauvazhimo, sho rizik third portfolio against the other є whistling at 4%, then the income of the lower tilki by 2%, the pidpriemstvu, yak pragne zniziti rizik, varto spiniti sviy vibri on another portfolio. The characteristics of the portfolio are shown in the form of the actual amount of the actual amount of income that can be accrued for you.

Controlling food

1. Characteristics of the main lines of investment and investment activities.

2. Type of investment dіyalnostі, що є prіоритетним для підприємства.

3. Perevagi that nedolіki method of clean tperіshnogo varmosti.

4. Zmist method viznachenny internal normi pribudku інвестиційного to the project.

5. Characteristics of the period of investment in the investment project.

6. The basic model, which is to be visualized for the purpose of pre-admission of oblasts.

7. Warehousing of the customs of the pre-institutional papa.

8. On the basic principles of visibility, the investor in the process of pribannya ta zberigannya tsіnnih papperіv?

9. Duration of the paperna.

10. Is there a certain degree of vicariousness for the analysis of managerial behavior by diversifying a portfolio of paperns?

The list of recommendations is recommended

1. Економічний аналіз: The Navy. Посіб. / MA Blukh, VZ Burchevsky; For Ed. M. G. Chumachenka. - K .: View of the KNEU, 2001. - 540 p.

2. Primostko L.O. Фінансові деривативи: аналітичні та облікові аспекти. - 263 with.

3. Fedorenko VG, Gojko AF Інвестзнавство: Підруч. / For the sciences. Ed. VG Fedorenka .- K .: MAUP, 2000. - 408 p.

4. Inventions in the promising industry of Ukraine: Monograph / VG Fedorenko, OF. Іtkіn, DV Stepanov та ін .: За наук. Ed. VG Fedorenko. - K.: Science. Svit, 2001. - 447 p.

Comments

When commenting on, remember that the content and tone of your message can hurt the feelings of real people, show respect and tolerance to your interlocutors even if you do not share their opinion, your behavior in the conditions of freedom of expression and anonymity provided by the Internet, changes Not only virtual, but also the real world. All comments are hidden from the index, spam is controlled.