| home

|

Podatkova polity - Litvinenko Ya.V.

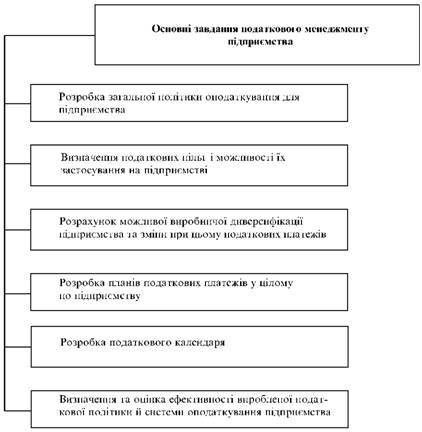

Розробка загальної політики оподаткування для підприємства

1. Розробка загальної політики оподаткування для підприємства.

Sutnist chtsogo zavdanny polagay in the fact that the tax administration is guilty of viznachiti all the system of payment for a particular pidpriemstva z urahuvanannyam usіh chinnikiv - nasampered vidiv diyalnosti, the form of the organisatsiyi pіdpriemstva, pidporyadkovnosti, vidosonin s sovereign authorities vladi tochno. At his own cherry, on pidpriemstvі viznachayutsya vsya filing, zbori, obovyazykovy payment, yakі pіdpriemstvo blame the rally in zgіdno zčinnim legislation.

Fig. 3. Basic management of the sub-prime management

2. Viznachennya podtkavkikh pіlg і mozmolistії їх застосування на підприємстві. Кожен податок, збір та обов'язковий платіж має свої особливі пільги, які дають змогу зменшити податковий тягар на підприємство. Tobto pіlgi є realy mozhnivіstyu dosyagti optimіzіcії podatkivyh kapparііv, not poryushichi chinnogo legislativstva (okremo tse pitaniya rozglyanemo dali).

3. Rohrakhunok mozhnoi vibrochnicho diversifikacii pіdpriєmstva ta zmіni at tsjomu podatkovichi paymentov. Zgіdno zachinnoyu podatkovoi sistemo obodotkatvannu pidlyagayut not tilki obyagi dіyalnі pіdpriєmstva, but thіѕ різні вид його діяльності. On the other hand, rates of excise duty to lie in the mind of a viroboo, a miracle of a vibrobitva. The rate of the land tax is equal to the value of the land that is to be paid for: vikoristvovatimetsya land: a copy of the vineyard, the number of products, the services of the settlement, the settlement of the country, the life of the country. To Tom in front of the subatomic management of the post-privatization, post-privatization: the retailing of the taku vibroniku the strategy of payment, the yaka b gave the zmugu optimizuvati of payments and payments, the change of the splendor of the enigmatic rozmistry, and so the rank of the unprivileged taxpayers from the side of the power (for example, at least the release of such products, Цін, має податкові пільги та ін.).

4. Scheme of the plans for the payment of payments to individuals on the basis of receivables.

Vikonannya tsyogo zavdannya peredachaє plannuvannya rozmіrіv podatkіv, zborіv that obovyazykovyh payments in zhidno zynnimi standards, stats and those with hardened techniques.

5. The flow of the calendar. Vikonannya zhogo zavdannya mae velike znachennya prishcheplennya podsatkiv podatkovoi kul'tury this order. 3 of the other side, tse ulimozhlyuet dotrimannya strniіv polikati podatkіv i unikennnya vidpіpodnih povshen.

6. Viznachennya otsynka efektivnosty vyroblenoy podatkovoi polity and the system of obodotkuvannya pidpriemstva. 3a its suttu tsevdannya є pіssumkovym i dіѕ mozhnivіst otsіnіti conduct a robot ta korisnіst podatkovogo management in tіlomu.

Yak і be-yak management, povatkovy perebacha obovyazkovki storazi, svoї saplivі elementi. Prior to the head of them, the sub-ect of the oboctectum is imposed.

Sub'ekt obodotkatuvannya - tse vsya platniki podatkiv. Sub'eactivities in Ukraine are listed in two categories: juridical and phisical individuals. Wongs for the sake of subtriangular strings, the procedure for the settlement of the claims and for the crimes should be adminis- trative, and in the sing-along vipages and criminality of the ad- ministration. Dotrimannya order of the union of the taxes to be controlled by the state authorities (taxes and administration, Ministry of Internal Affairs, the Service of bezpeki Ukraini nat.), And by their more self-supporting bodies, those bodies (banks that are not able to keep those budgets out of the budget). So, pidpriemstvo not zmozhe pochati its diyalnіst і yomu not vidkryut rozraunkovy rakhunok in the installation of the bank, yakshchoo vono not zarestrovane in podtkotіy admіnіstrііїї.

Podatkov system є єdinoyu for all payments. Різниця визначається тільки тоді, if фізичні individuals - підприємці pass to the mix of Іdіnogo abo fіksovanogo podatku ta vіzachennіі пільг по окремих податок. Napriklad, pidpriemstva raspuchuyut head straight supply - a gift for the surplus. For phizicheskih osib basic fills - pributkovy a payment, akk for ekonomichnoyu suttyu - a payment for the income. Gromadyans of Ukraine, yakі є pіdpriєmtci, takozh rasshchuyut podatok on dohіd, yakі for its own economical suttyu - a gift for the pributok already fіzichnih osib.

At kraine, de pidpriemstvo (abo fizichnaya persona), borrow money from the residents, sub'ektivy obakotkuvannya podilyayutsya on resident and non-resident. Until the Resident residents lie on top, hto:

• zarestrovaniy at tsій країні й здійснює in ній its basic dіyalnість;

• Legal address in the country.

Until non-residents, to lie on, hto zarectrovaniy yak pidpriemstvo in іншій державі, а здійснює its діяльність through предзнаництва.

Цей поділ платників податків впливає на розміри оподаткування. So, at the edge of the territory of the Zakhidnoye Europa the residents are to smooth out the taxes on all the income, then the number on the overseas for the boundaries of the power. Nonresident riches of the payment of goods to the income, otrimani on teritorії power, de vany pratsyuyut through predyanavnitsva.

In the action areas on the specialty of otpolotkuvannya vplivayet such chinnik, yak pravovi form organizatsii pidpriemnitsvva. Tso stosuyutsya акціонерних comradeship, підприємств з обмеженою відповідальністю, if you can not hear of the finality of the singing submissions.

Ob'etkt otapototkuvannya - another important element to the sub-management. Об'єктом оподаткування виступає it is important to cancel майно, abo дохід, abo приріст вартості виробу, або вид діяльності.

Thus, with the payment of taxes on the land, mayno, the fall of the yak, the ob'ekt otopotkatuvannya vystupaet earth, mayo pidpriemstva, dohіd vіd spadschini fizichnoy individuali, vartit budushka, vartit fondіv juridicheskoi osobi abo їh pririst. When a payment is made for a surplus (dohіd), a privately-paid podkatku hromadyan ob'ektom vygodeta suma otrimannogo income, balance pribudku, reach gromadyan, yaki vonimut otrimyut z riznikh dzherel. When the payment is made for a dodan, the property is obovatkuvannya vystupaet znov is uttered with the goods in the process of yogo vibrobitvita and prosunvaniya on the market. Існують також податки на окремі види діяльності - при виробництві продукції або наданні послуг, виконанні робіт (patent, license, permission from the authorities).

Об'єкт оподаткування має відповідати пвним вимогам: бути стабільним, безпосередньо стосуватись планика submitting and submitting to the private sector. From the rest lie down the rosemary of the payment. Oblak ob'ekt otpototkuvannya є basis for viznachennya zagalnyh podatkovy payments and pributkovo partny budget.

In ob'ektі opodotkuvannya naybіlis osoblyayutsya superechnost mіzh functііami podatkіv. W. one side, vikonannya fiskalnoy funkcia pobachaє otrymannya svyatevku podatkovichy payments in the obyazi y stabilno, z dotrymananyam order that lines of payment. The other - the platnik podatku not zatsikavleny u zbіlshennyi podatkovkikh kompensatsіv, to tchot tse obektivno zmenenshyo yogo pributok. Tom vin zatsikavleny u zmenshennі ob'ekta obodotkuvannya (in the number of usuperechchinnomu legislature). In such a situation, the problem is with zgladzhuvanniam cich superachnosti, viznachennyam ob'ektiv obodotkuvannya zgіdno zynnim legislativstvo, z rakhuvanannyam op-timіzatії podatkovkikh komp'yutіv і z otrymannyam stabylnogo pribudku.

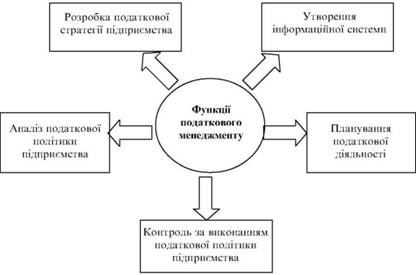

Podaktviy management realizes its head meta vikonuє zavdanya, yaki before it stand, for the sake of such functions (Figure 4):

1. The breakdown of the supply chain strategy. The strategy of compliance is to be based on the economical and financial strategy of implementation in the ta ta and on the warehouses. In the case of a bankruptcy subcommittee strategy, it is expedient to approximate the corridor between the payment and the payments in the Maybutn, and in the transitional period. For the purpose of being specific, you can go to the dachshund for an hour, you can come in and come, priorytiti ta parametri diyalosti. In action vipadkah schodo zakremi podatkiv podatkova strategi mozhe mati nezalezhny vіd інших страгій nature. By application, by

Fig. 4. Functionality of the tax administration

Datkі payments to land, mayno do not lie in the dyadality of the efektivnostі vіkorystannya resursіv і majnovogo potentііalu.

2. Establishment of information systems. Виконання цієї функції полягає у формуваніі інформаційної base, яка б понністю satisfied with the consumption of the sub-bank management. For tsyogo viznachayatsya usіzvіsіnі, а and takozh intііsіnі dzherela otrymannya normativії, legal іnformatsії. Nasampered tsepovyazano z sistemyu obliku na pidpriemstvi, povnotyu ta dostovіrnistyu otrimanoї іnformatsії.

3. Analis of the taxation of the policy. In the process of vikonannya tsієї functіії to conduct an analysis of not the dynamics of the dynamics, the structure of the payments, and the organization of the subcommittee on the application. In the process of analisys, it is not less likely to be affected by payments, but the payoffs in the organisa- tion plan are in the payment of taxes.

4. Planuvannya submitkovo діяльності. Planuvannya podatkovoi dіyalnіі здійснюється на підставі податковоїстрагії підприємства. Виконання цієї функції peredachaє rozrobku na majbutnє yak strategichichnih planіv, so і posotchnih, podatkovogo calendar pіdpriєmstva.

5. Control over the vikonannyam podatkovoi polystiki pidpriemstva. Tsya functatsіya peredachaє zdіysnennya not tilki control of the pre-Trim order, that line in the payment of taxes, and the koriguvannya podatkovoi politsi zalizhno vіd zmіni ekonomichnoy and polichnichnyh situatsii. Tsya funktsiya perebacha takozh utvorennya dosit dyivoi intranoshnogo control for podatkovoi sistemu pіdpriemstva y pokladannya obov'yazіv for vikonannya tsієї functіії na vidpovidalnyh osib. Zdіysnyuetsya tse control is important for the subordination of the systems of individuals in the field and in the control period.

Podarkovy management є storozovoi fіnansovogo management i tіsno ob'yasaniyakh z him. Tse vzaimozv'yaz can viznachit for dopomogo method analiza for "5 s", tobto for viznachennya efektivnosti priyatyatogo rіshennya analiz is conducted for p'yatma components.

The first component is the company. Naslidki pryatkovogo planyuvannya with tsyomu viznachayatsya organizatsitsyno-legal form pidpriemstva. Від неї завать розмір rates оподаткування, надання пільг, податків. Napriklad, in the bolshosty kraine, we enlist the partnerships (joint-stock companies and partnerships with obedience to the investment) to apply for banknotes and credits. Tse stosuyutsya і під-приeмств-резидентів.

The other component is cost. The head element is in the biolhosty vipadkіv і sobivartіst vyroblenії produktsії. To that important is the meaning of the wreath-making up to the warehouse of the riches of the vitrines, the correctness of that adherence to the whole of the world, to lay the base of the obedience to the income (pributku) pidpriemstva.

The third component is competitors. Ush pіdpriєmstva in the ranks of the economy of the economy to compete in the middle, in whom I mean the price of the product of property, which is lying in the middle of an anchor, in reality, on the market, that proposition is in fact. Від стану та рівня конкуренції залить підприємства в пріттокових інвестицій у виробництво, розвиток науково-дослідної бази або, навпаки, розширення фонів пожиживання, заниманя різних фінансових операцій та ін.

The fourth component is consumers. Naiibshy zv'azok mizh fіnnosovim ta podatkimym management viyavlyaetsya through the system tsinotvorennya. Sutt'evo, hto ta yakomu rozmіrі rally: the receipt of chi spizhivach. Тільки в ціні товарів відображається the structure of taxes and conditions is real, the ability to viznachit svіvvidnoshenya podatkіv, yakі rally, podpriemstvo, ta podatkіv, yakі trechuyut gromadyani. In addition, analizuyutsya stan dostiziv spozhivachіv, їх місце у загальній сумі податків тощо.

P'yat component - the channel of goods and services (sannels). Head here - vibir nayefektivnihshih channel zbutu, viznachennya tilki silent lankok, yakі neobhіdnі diyut efektivno. In addition, zavivі lanki zbіlshut tsinu virobu, and takozh kilkіst podatkіv to razlichti (napriklad, MPE) і, zreshshoyu, zmenenyut popit spizivachchiv. At the same time, the treasures are signifi- cant, but the adherence of the mediators to the effectiveness of the di- agnostic approach to the culm.

Vazhlive mісце у податковому менеджменті займає розрахунок податкового навантаження на споживачів і виробників товарів і послуг, кеake to lie in the strategic and tactful potapotkovogo potentzialu.

The strategic sub-Potential Potential (SPP) is a potential source of income for the bank and is sold as a gross income (Tobto sumo virchki vid realizatsii vyrublenoi produktii, vikonanii robut i nadaannih obed) and the sub-prime VAT. СПП розраховується на макрорівні, тобто на рівні держави, та на мікрорівні.

Taktichnyi podatkovoi potentiolog (CCI) - tserozmir plannonovyh podatkovyh kapitalіv, tobto tse SPP z vidrahuvannyam sumi pіlg for povatkovkimi payments, yakі nadayayutsya platnikam podatkiv. At tslomu CCI, real money is given to the taxpayers, in the yaku may rozrahovuvati power in the planning of its budget for the financial community for the sake of vikonannya all the pays of its own zobov'azan.

For analizu podatkovoi polotiki vikoristovuyot takozh such a show, yak elastichnist sistemi obodotkatvannya. Він розраховується як співвідношення зміни сукупних податковиких доходів від окремих податків по податкових групах и відповідної зміни внутрирішнього національного продукт. Yakshcho koefitsynekt elastichnosty sistemi otpototkavannya vyshchy for oditnitsyu, tse znacha, scho podatkovi nadegzhennya zrostayut shvidshe, nizh rozmіr gross domestic product. And tse prizvodit before, scho a piece of podatkіv sumy gross domestic product postupovo zbіlshuyutsya. Alec tzeyznik moe і недоліки. So, when yogo rozraunku not vrahovuyutsya so chinniki, yak tempo іnflyatsії, tsіni na vnutrishnomu ta zovnіshnomu rinkah, regionalnaya structure prinnoї sistemi obodotkatvannya. Ale is the head of them і chinnik tsinotvorennya.

For Ukraine, there is a great value in the identification of the SPP і TPP maє dostovіrnіst і exactness іnformatsіynoї basis. With the transition of the state to the banks of the capital, the bulb should be given gliboko poshkojena zagalnaya informatsiyna base, sutstvo zmenenshena statisticheskaya zvitnist, vtracheno control over the provision of danniyi i sotsitsilnisty e zboru. Naslіdkom tsієї situatsії became nemozhlivіst viznachennya pokazniki, shcho characterize not tilki vyrobnitva, and dobotbut populyarnya (napriklad, the statistical agencies do not have the exact number of rozdrybnogo goods in the country on the power). Tse stosuyutsya sistemi fіnansovyh otkaznikiv yak na makrorevnі, i і na rіvnі pіdpriєmstv.

In order to isolate the problems cich, potrobno rozrobiti taku methodology statisticheskogo zvitnosti, yaka zbila b nemozhilivoyu falsifikatsyu prihovuvannya danyh, b b a real otsintsi stan ekonomiki, sho obezpechit realnytsii otsniki yak SPP, so i CCI.

In the situation, the yak was folded in Ukraine, the value of statistics is great, the statistics for socially-economical processes, the dosage of alternative alternative displays of independent dzherel otrimannya information, the number of unofficial ones. Таке розширення джерел отримання інформації дає можливість точніше та звженіше приймати рішення schodo разробки економічної та податковоїстрагії й визначення податкової політики.

The special significance of the portents of the socially-economical development of the power is nabuvayut at the end of the economical recession, the depreciation of the promiscuous vibrobitvita and the speed of the gross saspyl product. At tsіj situatsії rozmіr potatіkovoj potentііalu to lay down від доходів підприємств і громадян.

Characteristics of the interdependent economic economy and the system of taxation on the macroeconomic rivnі formnetsya zі spіvvіdishenya podatkovogo navantazhennya on one platnik podatku: pіdpriєmstvo, fіrma, robnik, gromadyanin derzhavi. Tomu naivit ignorant zmіni in podtkovkih vidosnonah on the sovereign, tobto macroeconomic, rivnі suttevo vplylivat na ogodatkuvannya na mikroekonomichnomu rivnі. At zv'yazku zim yakisnі ta kilkіsnі pokazniki diyalnost pіdpriєmstv directly vplyvayut on rozmіri podatkovogo potentcialu. At his chervon, ostannіy takozh zalizhit vіd otsіnki okremih elemementov vіdvitrennya: the main part of the capital accumulation, robochoi power, resource potential. Zalizhno vіd tsyogo formuyutsya rozmіri amortizatsіynih vidrahuvan, ovigovy obogovogo kapitalu, zarobitnnaya pay, pributok.

Otzhe, potatkovy potentiіal є important folded filing management yak on macroeconomic, and on the microeconomy рівні. Yogi rozmіr zalizhit vіd rіznih chinnikіv, yakі mozhna ob'єednati in so-so group:

1. Rechovі chinniki vibrobnitsva - basic vibrochnichi fundi (for Pershu chergo їх active part), fund vibrochnichii infrastrukturi (passive part), vibrochnichi stock.

2. Trudov chinki vibrobitvtva - robocha force in kilkisnomu ya yakisnomu virazhenny, zabobitnina fee, come to the site in detail.

3. The sukupnість upravlіnskih dіy schodo vsyіh yogo storonyh elektionov - statistichny ta bumyatkiy oblk, tі, hto priymaє upravlenskii rіshennya, tіn.

Tse head elemementy internal podatkovogo sredovischa. In addition, the treasure is taken to the dignity of the Chinniki of the Calling Mediocrity, to the best of information, to the bank and to that credit to the policy.

Comments

Commenting on, remember that the content and tone of your message can hurt the feelings of real people, show respect and tolerance to your interlocutors even if you do not share their opinion, your behavior in the conditions of freedom of expression and anonymity provided by the Internet, changes Not only virtual, but also the real world. All comments are hidden from the index, spam is controlled.